I’m no fan of the Federal Reserve. After three decades of watching their every move with a critical eye, I’ve come to a stark conclusion: it’s time to dismantle this institution. For 111 years, the Federal Reserve has been at the helm of America’s economic ship, and frankly, the results have been less than stellar. It’s a bold statement, but one grounded in a deep-seated belief that markets should be free — truly free. This means interest rates and money supply should be dictated by market forces, not a central body.

When Alan Greenspan held the reins as Fed Chairman, Wall Street bestowed upon him the moniker of ‘The Maestro.’ The title was not for his finesse in orchestral arts but for his seemingly adept control of the financial markets — stepping in with a saving grace whenever Wall Street so much as sniffled. This modus operandi set a precedent, one that every Fed Chairman since has seemingly adhered to. The formula is almost painfully predictable: Wall Street falters, the Fed swoops into the rescue.

Over the past 16 years, this pattern has manifested through various iterations of Quantitative Easing, all aimed at ameliorating the blunders of the Great Financial Crisis. But the looming question remains: Are we truly better off? How do we even begin to define success in this context? By my measure, the continual interventions have not only failed to address core economic issues but have compounded them. The more the Fed intervenes, the more it distorts what should be the most critical price in capitalism: the price of money.

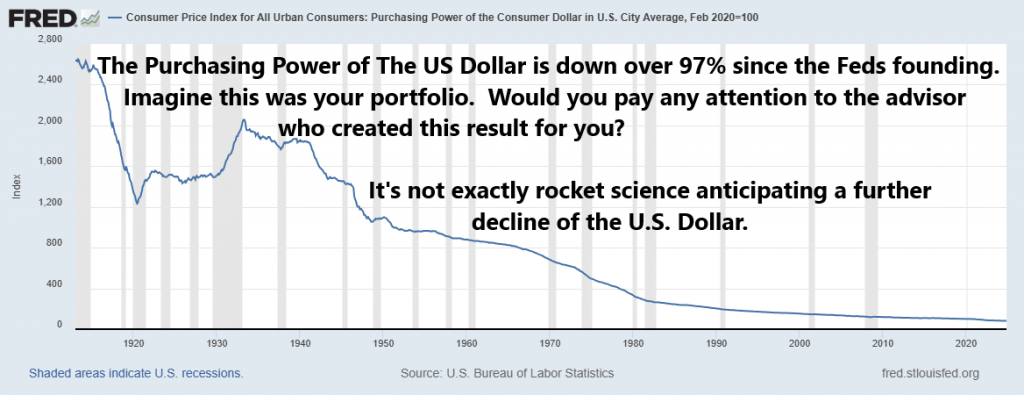

Since its inception in 1913, the Federal Reserve has presided over a staggering 97% decline in the purchasing power of the U.S. dollar. One might wonder, how can such a precipitous drop be seen as anything but a profound failure? If a financial advisor were managing your portfolio and it plummeted by 97%, would there be any trust left for that advisor? Unlikely. Yet, we continue to entrust the Fed with the helm of our nation’s monetary policy. This stark erosion of value under their watch is the crux of why I argue that the Federal Reserve is not just out of touch but is primarily focused on preserving its own institutional power rather than the economic well-being of the nation.

The purchasing power of a nation’s currency isn’t just another economic statistic; it’s a vital indicator of a country’s economic health and stability. It impacts every facet of economic life, from the prices of groceries to the real returns on savings. As purchasing power erodes, so does the wealth and economic security of every citizen who relies on that currency. By continuously devaluing the dollar, the Fed has not only diminished the individual’s capacity to save and invest but has also jeopardized the very foundation of our economic future. This persistent decline signals a disconnect between the Fed’s policy interventions and the long-term economic prosperity of the United States. It’s a sobering reality that questions the Fed’s role and effectiveness, spotlighting the need for a reevaluation of how we manage our nation’s monetary affairs to safeguard the future rather than jeopardize it with short-sighted policies.

One of the enduring consequences of Greenspan’s policies at the Federal Reserve can be likened to a parent who consistently refuses to discipline a spoiled child. By repeatedly bailing out the financial markets whenever they showed signs of distress, Greenspan inadvertently taught Wall Street a perilous lesson — that no matter the recklessness of their financial behavior, the Fed would always come to their rescue. This lack of accountability has fostered an environment where financial institutions continue to take outsized risks, secure in the knowledge that they operate under a safety net generously provided by the central bank. Just as a child learns to misbehave without fear of repercussions, the financial markets have grown accustomed to operating without the fundamental discipline that risk should naturally engender.

Any introductory finance course will tell you that the cost of money — interest rates — is fundamental and sacred. All changes in prices everywhere occur when the cost of money changes. It dictates investment decisions, consumption, savings, and broadly, economic well-being. Yet, when this price is artificially suppressed, the repercussions are dire. The outcomes are not just poor; they are gruesome, leading to misallocations of resources and unsustainable bubbles in asset prices.

What we’re witnessing is a system that strays far from the ideals of free market operations, embodying instead a hybrid of the most detrimental aspects of politics and centrally planned economies. This isn’t capitalism; it’s a façade, a system propped up by the very institution that purports to safeguard its health. The greatest threat to the Federal Reserve today isn’t external shocks or fiscal imbalances — it’s the concept of a truly free market in interest rates. A return to such a system would strip the Fed of its power to manipulate, revealing the true state of our economy, for better or worse.

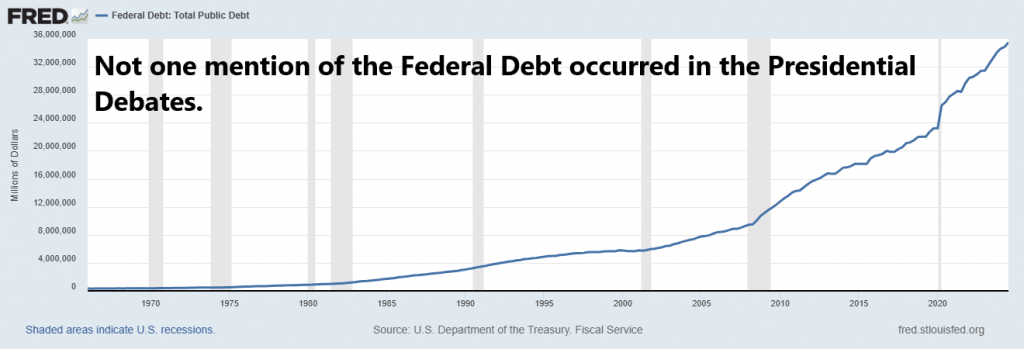

Did anyone else catch the glaring omission in the recent Presidential campaign debates and podcasts? Not a single mention of the national debt or its skyrocketing trajectory. It’s as though this monumental issue, one that defines the economic stability of our nation, has vanished into thin air — or maybe I missed a crucial memo announcing its resolution. But alas, the debt remains, silently swelling in the background, ignored by political discourse yet burgeoning with each fiscal year.

Is there a plan to pay back the national debt?

Will the United States default on the National Debt by simply paying back U.S. Treasuries with inflated dollars? After all this is the recipe that every kingdom and out of control government has used since the beginning of time.

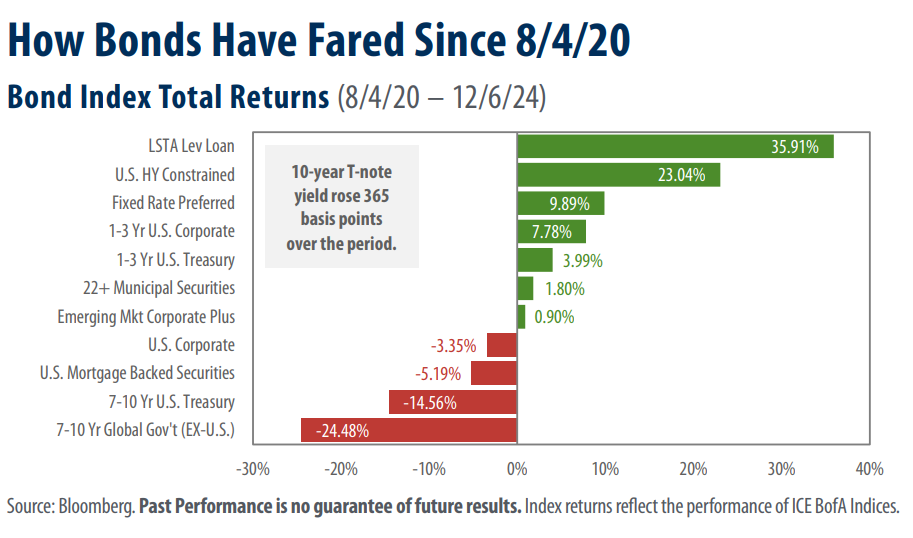

The returns on all the different types of Debt instruments have been completely toxic since 2020. That fabric must change if we are to see health and sanity return to the financial markets. As you study the performance metrics on the debt market since August 2020, subtract for roughly 20% inflation. Regardless of how you slice it – sovereign debt is TOXIC.

These are very reasonable questions that any investor would want to know the answer to.

Below is a chart of the U.S Treasury market over the last 4 years. Post-Pandemic. The world sovereign debt market is over $300 trillion in size.

Does the Treasury market look healthy to you?

Yet our leaders at the Fed talk about how strong resilient our economy is?

Question: How can you have healthy financial markets when the Treasury market is toxic?

Question: How does the government fund operations in a market environment where no one buys their debt obligations?

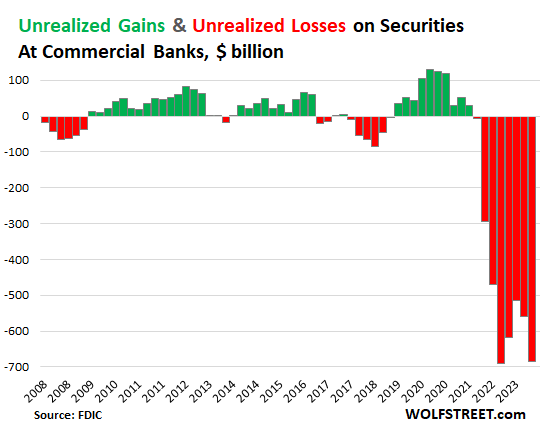

If the economy is so strong and resilient can someone explain to me the following chart from the Federal Deposit Insurance Corporation that shows bad debts at Commercial Banks are 15 times larger than they were during the Great Financial Crisis? Look at how these losses explode in 2020.

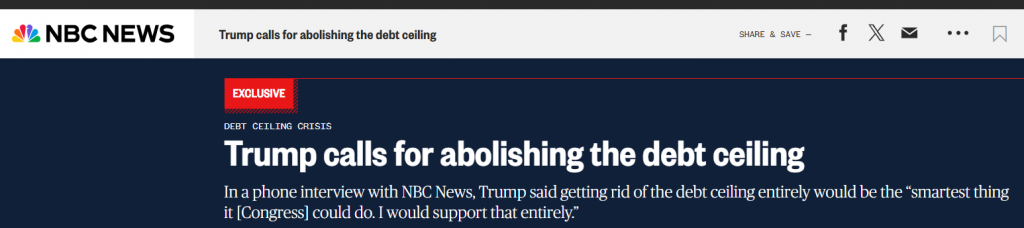

Question: Did you see how the incoming administration is planning to address the debt ceiling?

The Congressional debt ceiling acts as a statutory cap on the amount the federal government can borrow, ostensibly to restrain governmental spending. Each time the ceiling is approached, Congress is forced to decide: raise the limit to accommodate further borrowing or address the fiscal behaviors necessitating this increase.

The debt ceiling’s role as a fiscal brake is crucial. It compels lawmakers to pause and consider the sustainability of current spending paths and the long-term implications for future generations. However, its effectiveness is contentious. Critics argue it has become a political tool used more for dramatic brinkmanship than actual fiscal responsibility. The routine debates and subsequent raises or suspensions of the ceiling highlight its paradoxical nature: it is intended to limit spending, but in practice, it often just marks the continuation of increased spending and debt accumulation.

Therefore, while the debt ceiling aims to safeguard against fiscal irresponsibility, it serves more to spotlight the ongoing struggle between spending desires and fiscal constraints than to effectively curtail spending itself. The challenge lies not just in maintaining such mechanisms but in upholding the discipline they are designed to enforce. What is concerning right now is that we are considering doing away with the debt ceiling and are convincing ourselves that this is a good thing for the health of the financial markets and the country.

Is this the Department of Government Efficiency (DOGE) in action? If the debt ceiling limit is eliminated, currency debasement, which is a guarantee, will shift from gradual to EXPONENTIAL as the government spend with absolutely nothing in place to suggest restraint.

As we pivot from this baffling oversight to the policies being championed by President Trump, the concerns only deepen. The President-elect has openly advocated for negative interest rates and a weaker dollar.

Essentially, this means pushing down interest rates even further — beyond the zero bound — and deliberately diluting the value of the U.S. dollar even further. This strategy, ostensibly aimed at boosting economic growth by making American goods cheaper on the international market and encouraging borrowing and spending, may seem attractive on the surface. However, the implications of such policies are far-reaching and fraught with peril.

You don’t need a front-row seat to the economic arena to predict that this path leads to a precarious end. A strong currency has historically been a hallmark of a strong country. It’s a straightforward metric, really. A currency’s strength is fundamentally derived from demand, which is bolstered by the stability and higher interest rates it offers. Higher interest rates attract savers and investors looking for returns on their assets, underpinning the currency’s value. While it is true that the U.S. dollar is strong in FIAT terms against other fiat nations, the entire fiat system seems like a house of cards.

When a country opts to suppress interest rates into negative territory, it risks eroding this very foundation. The immediate allure of cheap borrowing can quickly be overshadowed by long-term economic distortions. Moreover, a deliberately weakened currency might boost exports temporarily, but it also raises the cost of imports and can lead to inflationary pressures. This is not just an economic issue; it’s a matter of national security. Economic strength translates directly into geopolitical strength, and a nation that undermines its economic fundamentals might find itself compromised on the world stage.

In this economic playbook, where interest rates are pushed ever lower and the currency is devalued, the supposed benefits are short-lived at best. The real outcomes are a decrease in global confidence in the dollar and an erosion of the economic bedrock upon which our prosperity is built. If the strength of a country is mirrored in the strength of its currency, then the path to weakening that currency is, paradoxically, a path to weakening the nation itself. It’s a stark reminder that economic policies are not just levers to be pulled for immediate gains but must be managed with an eye toward sustainable strength and stability.

Rate cuts, a tool as old as the institution itself, were once seen as the Fed’s magic wand — wielded to stimulate borrowing, invigorate investment, and combat economic slowdowns. The principle behind this is straightforward: lower interest rates make borrowing cheaper, businesses invest more, and consumers spend more, all of which theoretically lead to economic uplift.

Historically, this approach did have its moments of apparent success. During recessions and downturns, slashing interest rates helped breathe life into the economy. These periods were marked by robust recoveries, where lower rates paved the way for affordable capital. It was seen as a masterstroke of economic manipulation, a way to steer the country clear of potential economic disasters.

But let’s pivot to the present. Today, we stand in a different era — an era where such traditional mechanisms are not just failing to yield the expected results but are, in fact, sowing seeds of long-term financial instability. The economic indicators today tell a troubling story. We are doing better than the rest of the world for sure but that is not a metric that I would consider to be very important. Despite aggressive rate cutting, inflation stubbornly hovers above target levels, economic growth is tepid, and wage growth is not keeping pace with the cost of living. It’s a cocktail of economic malaise that no number of rate cuts will cure.

Since the Great Financial Crisis what we have gotten is ASSET price inflation as far as the eye can see.

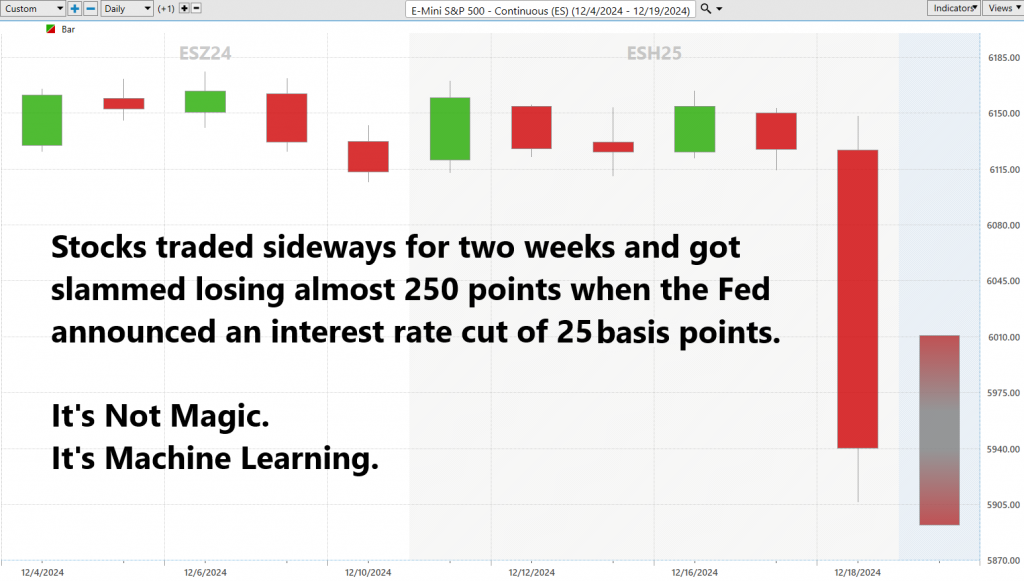

In 2024 alone, the Fed slashed rates by 100 basis points, yet what did we see? The market’s response was akin to a shrug, if not outright panic, as evidenced by the largest drop in the S&P 500 since the crisis of 2020. This wasn’t just a market correction; it was a market rebellion. Investors and analysts alike are increasingly viewing these cuts as inadequate responses to deeper systemic issues—like putting a band-aid on a fracture.

This leads us to a crucial point: the disconnect between Fed actions and market reactions is growing. Markets, it seems, have grown wise to the Fed’s playbook. The anticipation of cuts often leads to preemptive adjustments by market participants, thus diluting the impact when the cuts finally come. Furthermore, there’s a burgeoning lack of faith in the Fed’s ability to steer the economy effectively through interest rate adjustments alone. The belief that more money and lower rates can fix fundamental economic woes is fading fast, replaced by concerns over perpetual debt cycles and diluted currency value.

In an era marked by such critical scrutiny, the role of the Federal Reserve is increasingly questioned. Its century-old mandate of managing the economy through levers like interest rates seems archaic in a world where those very levers no longer yield the control they once promised. This prompts a compelling argument for a return to a truly free market system, where interest rates are set by the invisible hand of market demand and supply — not by the visible hand of a central institution.

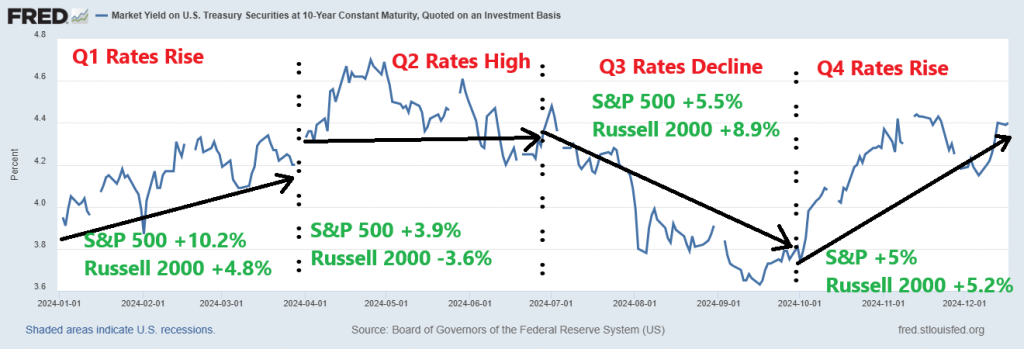

Let’s review the big picture financial events of 2024, quarter by quarter.

Below is a chart of the St. Louis Federal Reserve and the yield of the 10-year Treasuries. I have superimposed the returns of the S&P 500 and the Russell 2000 against this framework.

What can we expect moving forward?

My expectation is that the government has no choice but to continue to debase its currency. They will not call it that. But when you depreciate a currency, everything priced in that currency increases in price. This asset inflation has been occurring for years and masks all of the serious structural issues in companies and in the economy. It continues to promote the notion that you can solve a debt and spending problem by simply creating more debt and more spending.

Call me skeptical but that is how these government reports pull the wool over everyone’s eyes.

I don’t forecast.

I follow the trends as outlined by artificial intelligence.

Let me explain.

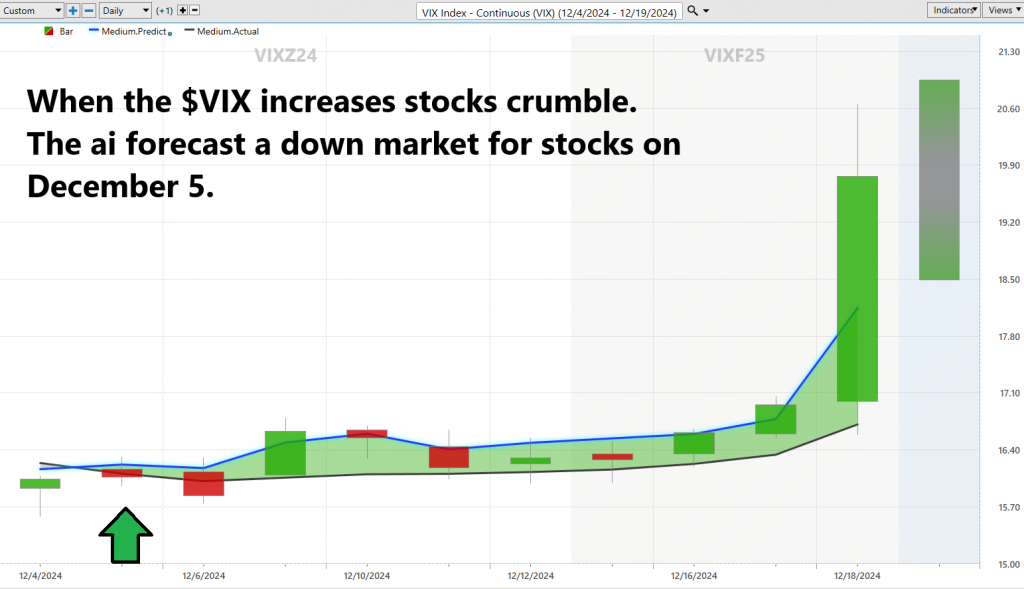

Here is a chart of the S&P 500 Index and the Volatility Index going into the Federal Reserve Open Market Committee meeting yesterday. Higher volatility is inversely correlated to the S&P 500 Index. When the $VIX is rising it is a strong warning that bearish storm clouds are gathering.

Observe how the artificial intelligence forecast anticipated the recent decline.

Here is the chart of the $VIX starting from December 4th.

Look at what happened to the stock market during the same timeframe.

I’d all like to see the new administration turn this muddled chaos into a roaring success story. Yet, while optimism has its place, let’s face it — the capital is a quagmire of unresolved issues, and without implementing genuine, logical solutions, the cycle of debt only deepens. Until we see a solid plan that doesn’t involve piling more debt onto our already mountainous heap, I’ll stick to my skepticism and hoping for political solutions to real structural economic issues.

Are you tired of hitting dead ends in your trading journey? Every trader starts with a dream of achieving financial freedom, but the harsh reality of the stock market often leaves many licking their wounds. The problem isn’t just about picking stocks; it’s about trading effectively in a world where risk is always lurking around the corner. Every day, traders face the daunting challenge of making decisions that can either make or break their bank.

Trading is no walk in the park. The emotional roller coaster alone is enough to send even the seasoned traders spiraling. Anxiety, fear, and doubt creep in with every dip in the market. And if that’s not enough, there’s the constant barrage of conflicting information, overwhelming data, and complex charts that make your head spin. It’s a battlefield where only the toughest survive, and unfortunately, emotions are often a trader’s worst enemy.

Now, imagine a solution that cuts through all the noise, emotion, and confusion. This is where predictive artificial intelligence steps in, your new trading companion. A.I. transforms the chaotic world of trading into a structured, data-driven battleground. It doesn’t sleep, it doesn’t fear, and it certainly doesn’t succumb to the whims of human emotions. Every day, A.I. performs top-level trend analysis, scours through mountains of data, and identifies potential trading opportunities with precision — effortlessly.

With VantagePoint’s A.I., you’re not just trading; you’re trading smarter and with confidence. This technology isn’t just about keeping up; it’s about staying ahead. A.I. arms you with insights that enable you to make decisions not just based on hunches, but on hard, analyzed data. It’s like having a supercomputer by your side, one that helps you navigate the complexities of the market with ease.

Ready to revolutionize your trading game? Join our exclusive webinar, Learn How to Trade with A.I., and unlock the power of artificial intelligence in your trading strategy. This is your chance to learn from the experts, see AI in action, and understand how you can apply it to achieve consistent trading success. Don’t let emotions dictate your financial future. Click the link, register for the webinar, and step into the world of AI-powered trading today!

It’s not magic.

It’s machine learning.

THERE IS A SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.IMPORTANT NOTICE!

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.