As I ponder the Federal Reserve’s actions on interest rates, I can’t help but recognize that I have seen this movie many times before. I know how this movie ends. The plot is always identical:

The Fed tightens.

The Fed tightens a little more.

The Fed tries to tighten a little bit more.

Something important breaks.

The Fed responds by changing policy and opening the monetary floodgates to start the cycle all over again.

The only variable in this process is how much time elapses until something breaks.

If you read the headlines of the financial media today many of the participants are cheering for something to break so that we can return to a low-interest rate policy once again.

But did low-interest rates really help or hurt us?

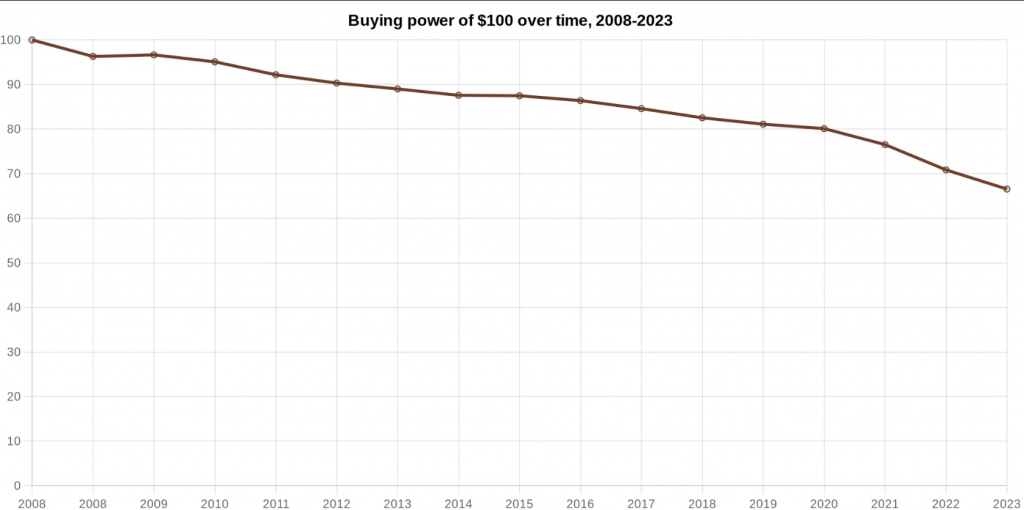

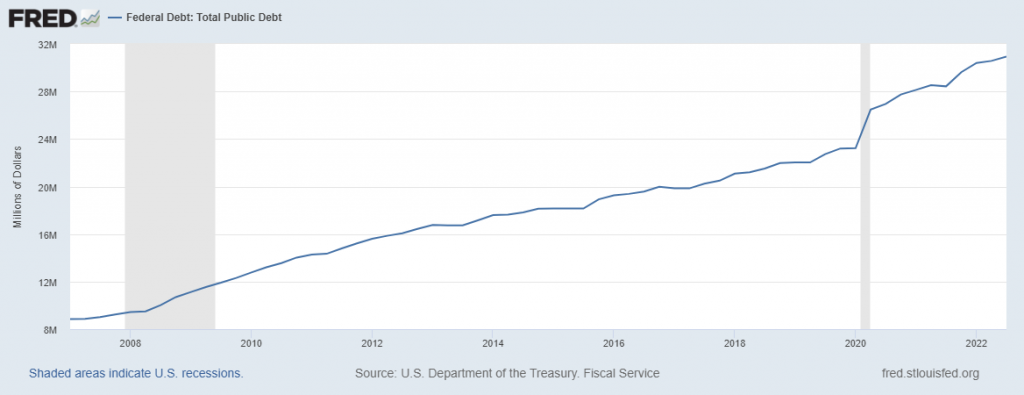

I like to look at where we have been and where we might be going because it certainly appears that it is a mathematical certainty that the government will continue to debase the currency. Since the Great Financial Crisis in 2008 the U.S. Dollar has lost 27% of its value. Currently the interest payments on the debt amount to over $750 billion where before COVID-19 they were around $350 billion. These two facts by themselves leave me very disenchanted with the Federal Reserve policy.

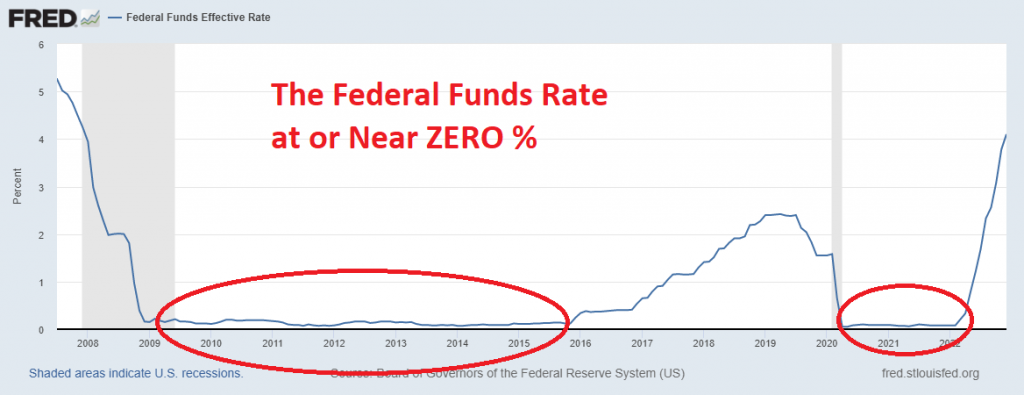

The Federal Reserve’s interest rate decisions are driven by the state of the U.S. economy. After the Great Financial Crisis, America was in a period of economic stagnation and deflationary risk. The experts and monetary authorities concluded that what was needed was intervention from the central bank. The unorthodox move to drop interest rates to zero or negative to stimulate activity had never been done before in a recovery period. This unconventional measure was intended to create an environment with greater financial incentives for lending and borrowing, thus increasing business investments, household spending, and overall economic growth. In addition to these short-term benefits, some economists posited that this may help break deflationary cycles and potentially result in long-term structural changes that improve market efficiency domestically.

Recently I was listening to a podcast episode with noted credit market expert James Grant of Grant’s Interest Rate Observer. Grant commented that the interest rates of the last 14 years were the lowest in all recorded history. That is quite a fact worthy of contemplating and thinking about. We have over 4,000 years of recorded history regarding the cost of money according to Sydney Homer and Richard Sylla in their book, The History of Interest Rates.

The “Too Big to Fail” policies implemented by the Federal Reserve after the Great Financial Crisis were based on a simple rationale: If a large financial institution were to fail, it would risk spiraling into an uncontrollable chain of failures for many other financial institutions. This in turn could put the entire U.S economy at risk, and so instead of allowing such an event to happen, the Federal Reserve designed a set of economic regulations that enabled these large players to receive government bailouts in order to prevent any serious fallout. This precautionary measure was thought necessary to maintain stability in the system – while avoiding further economic hardship and protecting taxpayers from having to bear the costs of an irresponsible banking system.

The Federal Reserve plays a crucial role in the modern economy and its ups and downs. The Fed is responsible for the creation of the boom-and-bust cycle, also known as the business cycle. Through its involvement with money supply, interest rates, and other economic levers, it influences decisions made by businesses and investors, which in turn affects investment demand, output, unemployment levels and general economic health. The expansionary phase of an economic cycle usually occurs when the Federal Reserve lowers interest rates to stimulate growth through increased borrowing and spending. During this phase, businesses are encouraged to make investments that can generate returns for their shareholders. However, when the Federal Reserve raises rates due to inflation or too much spending, investment activity declines leading to recessionary contraction.

The central tenet of capitalism is savings and the cost of money. Capitalism centers around the cost of money and its influence on how resources are allocated. When money is expensive, it becomes harder to borrow and acquire goods and services, making it difficult to maximize profits. In turn, the allocation of certain resources may be shifted away from businesses toward investments, such as stocks and bonds. On the other hand, when borrowing costs are very low, companies can more easily expand across a variety of markets, creating opportunities to buy up assets or increase production with larger scale capital investments. Overall, given capitalism’s focus on competing for profits through additional usage of resources, the cost of money plays a vital role in establishing the framework for how these resources will be used.

But when the cost of money is artificially manipulated and pushed to zero interest rates to promote the greater good, what is being practiced and promoted bears very little resemblance to free market capitalism. Now 14 years after the Great Financial Crisis we can draw conclusions of how beneficial or destructive the Zero interest rate policy was to savers, long term investors and the economy.

I am personally not a fan of the Federal Reserve. The Federal Reserve’s policies have played a major role in worsening wealth inequality in recent years. One of its major tools, a loose monetary policy that involves low interest rates and the printing of large amounts of money, has some devastating consequences. Wealthier individuals have access to capital and can exploit investment opportunities that arise from this loose monetary policy, creating large returns for them at the cost of those who struggle to invest or can’t invest enough to reap such rewards. Additionally, with lower interest rates, savers receive diminishing returns from their investments leading them to save less thus exacerbating wealth disparities. While these policies may be implemented well-intentionally, the fact remains that they disadvantage the poor while propping up those already well-off. Furthermore, when you recognize that debasement of the currency is a near mathematical certainty in today’s day and age you can’t help but be skeptical of the experts who claim to have the answers.

One individual who staunchly opposed the government’s rescue policy, including cheap money policies, during the financial crisis of 2008 was Esther L. George—President and CEO of the Federal Reserve Bank of Kansas City and a member of the Federal Reserve Board of Governors. Ms. George had a deep understanding that bailing out Wall Street would have devastating impacts on average taxpayers. In opposition to massive governmental interventions, Ms. George wanted private-sector institutions to fail in order for true market discipline to take place so that similar events could be avoided in the future. Unfortunately, her views went unheard as large bailout programs like “Too Big to Fail” were implemented, costing taxpayers billions of dollars while only increasing the power and size of large banks.

Also, Richard Fisher, former president, and CEO of the Dallas Federal Reserve Bank, was vocal in his opposition to this policy. He argued that it only served to reward those who had made bad decisions and put taxpayers at risk. Furthermore, he explained that excessively printing money to replace assets was inflationary and ultimately detrimental for future growth. In a 2017 interview he succinctly described his views when he said, “I am firmly against policies with benefits concentrated at the top, but risks diffused throughout society.”

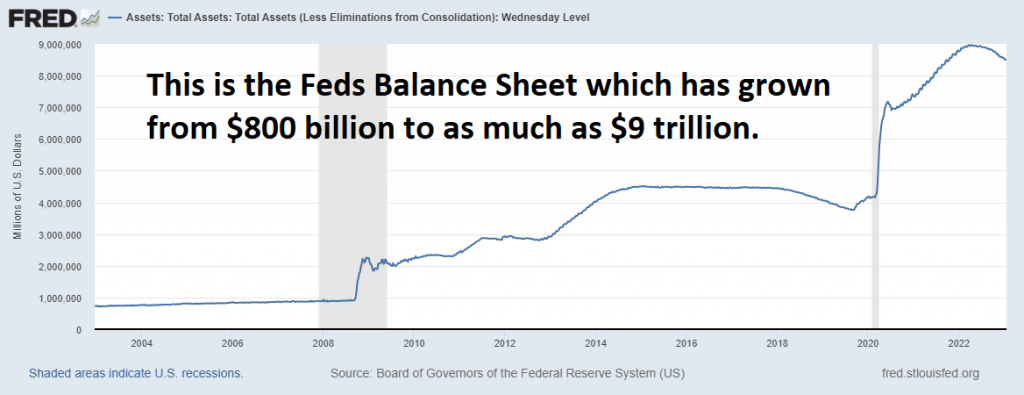

One of the horrific consequences of the Fed’s intervention over the last 14 years is the number of Zombie companies who could only survive today because of this access to cheap money. A zombie company is a business or organization with little to no active chances of survival. After years of mismanagement, instability, and unsuccessful attempts at reform, these companies survive only due to government assistance and bailouts. This assistance allows the company to remain afloat without significant changes being made in its operations or management. The term ‘zombie company’ was derived from the resurrection of insolvent entities due to external help instead of internal transformation. With many governments using the “Too Big to Fail” policy, especially after the 2008 financial crisis, there are now numerous zombie companies operating worldwide, notably in Japan, Europe, and the United States. Some analysts on Wall Street claim that 20% of the S&P 500 companies cannot repay interest on their debts from free cash flow. This trend has accelerated greatly as the Federal Reserve has been the buyer of last resort of these companies debt obligations.

2022 was the first year of financial tightening from an era in 14 years. Have you ever noticed that the word “stimulus” is no longer being used to discuss anything in the economy any longer?

Another very disturbing observation is that major financial media publications no longer refer to Credit Instruments as Treasury bonds. They now regularly add the adjective “very safe” Treasury bonds when writing about the credit markets. Treasury bonds, which are issued by the U.S. government, have always been considered one of the safest investment vehicles available but last year they generated losses in excess of 18% for those who purchased them. Not exactly very SAFE any longer.

All of these factors have led me to compile a list of the top unintended consequences in the economy resulting from the Federal Reserves Zero Interest Rate policy. In reviewing the economy of the last 15 years we can easily make some interesting observations and conclusions.

#1 – ZERO Interest rates are decimating savers and retirees as low-interest rates make it impossible to generate income safely on their savings. By keeping interest rates low, those with savings are deprived of the opportunity to grow their incomes through conservative, secure investments such as savings accounts. For many retirees without large employer pension plans, low or no return investments may make all the difference in terms of allowing them to maintain their desired lifestyle during retirement. Thus, while low interest rates may be beneficial to some, they can cause real financial hardships for savers and retirees who have worked hard throughout their lives to build a healthy retirement fund.

#2 – Zero interest rate policies encourage savers and retirees to take excessive risks in markets seeking higher returns than what would normally be available. This is unhealthy to the individuals and the economy as a whole.

#3 – Zero interest rate policies encourage over-indebtedness as low-interest loans make it cheaper for households and businesses to borrow. Low or zero interest rates have the potential to have a damaging effect on debtors. Although people and businesses might be enticed to take on more debt due to the low rates, they may find themselves in an even worse position if rates eventually do rise. This can leave them over-indebted and unable to pay off their mounting debts. Furthermore, when interest rates are close to zero for a long period of time, it can lead to significant losses for those relying on their savings as a form of income, thereby resulting in less money available for spending and investment.

#4 – Creating moral hazard. Businesses and financial institutions take on more risk than they otherwise would operating under the belief that the Federal Reserve or the U.S. Government will bail them out if events go awry.

#5 – ZERO interest rate policies disrupt the normal functioning of money markets and other short term funding markets. Low or zero interest rates effectively pull the rug out from under a healthy money market. Rather than encourage people to save and invest, low or zero interest rates minimize any potential returns on savings and investments, making it difficult for families to build effective financial portfolios. This disruption negatively affects not only consumers but also the banks, which depend on higher interest rates for profit in their loan portfolios. This can lead to more risk-taking by the banking sector, as institutions attempt to garner profits from additional sources when returns on loans have been drastically reduced. In this way, low or zero interest rates can create an unsustainable environment in which major shifts are needed if money markets are to remain stable long term.

#6 – Zero interest rate policies create massive stresses for PENSION funds who are incapable of generating adequate returns to pay pensioners. Low and zero interest rates reduce the returns on investments by pension funds and make it more difficult to meet their objectives. This puts pressure on them to take on more risk in order to generate greater returns for future liabilities, which increases their vulnerability during times of financial instability. When low or non-existent interest rates persist, pension funds are likely to struggle to remain sustainable and fulfill their obligations to retirees over the long-term.

#7 – Zero interest rate policies create asset bubbles. Low interest rates make investing in certain high-yield assets more attractive to the market, and this influx of new money can create a situation where asset prices skyrocket. This rapid escalation in value is known as an asset bubble and it can be seen in many sectors, such as real estate, stocks and crypto. When investors flock to these assets, due to the low interest rate environment, they often bid up the price until it reflects a level far higher than its fundamental worth. Eventually, this bubble bursts when investors realize that they have overpaid for the asset and sell off their holdings which leads to a sharp fall in price. The end result is that what seemed like an attractive opportunity at first can quickly become a devastating loss.

#8 – Low or zero interest rates present a major problem for the banking sector. Banks must be able to make a profit from the interest rates that they charge customers in order to remain profitable, so when those rates drop too low or become nonexistent, it restricts the ability of banks to make profits and can even sink them into financial losses. Further compounding this issue is the fact that many banks are large enough that falling into such a deep hole could have a ripple effect on the larger economy. Low or zero interest rates also reduce liquidity, as customers have less incentive to store their money in bank accounts with no accompanying return of investment. This form of restricted activity further reduces their ability to make profits, presenting yet another challenge for the banking sector success.

#9 – ZERO interest rates Increase the probability of increased government debts and deficits – Low or zero interest rates increase the probability of larger government debts and deficits when governments are unable to pay off their existing debts, particularly when they have overspent in the past. When borrowing costs are low, more debt is taken on to finance current and potential future actions by a government, including infrastructure projects and other investments. The problem occurs if the economy does not grow as quickly as expected, creating a possibility for rising long-term liabilities and unsustainable deficits. In this case, governments must respond with fiscal consolidation such as austerity measures and tax increases. This could be a difficult decision in light of economic challenges; however, it is necessary to avoid significant economic decline from piling up even with low interest rates.

#10 – Zero interest rates Increase the probability of sustained inflation – One of the major problems with a low or zero interest rate policy implemented by the Federal Reserve is that it can lead to inflation. This is because there is a surplus of money in the economy due to increased investments, but not enough productive outlets for where this money can go. As a result, prices tend to increase across the board and unevenly, leading to an overall decrease in purchasing power. Additionally, a longer period of low interest rates could cause people to act recklessly and take on more debt than they can actually afford. When this happens, consumers become overextended with their loans and risk defaulting. This can have serious implications on the overall economy since banks tend to increase their lending standards as debt defaults start rising, cutting off access to new credit and further reducing economic activity.

These criteria form my basis for evaluating the effectiveness of the Fed.

It can be impossible to determine the overall effectiveness of the Fed’s zero interest rate policy. After all, it is impossible to know how much worse or better off the economy would have been had the policy not been implemented. But what is supremely frustrating for me is the association many in the financial media make in trying to equate the health of the economy with the health of the stock market. While it’s true that healthy economic growth does fuel stock market success, performance on Wall Street does not represent an accurate representation of economic health, or lack thereof. Economic data provides an overview of trends in employment, wages, borrowing habits, disposable income and more which should all be considered when evaluating current conditions—not solely relying on fluctuations in stock prices.

For me, what the Fed has done is contributed to massive volatility in the stock market. This volatility discourages long-term investment and encourages short-term speculation. In its efforts to manage the economy through monetary policy, the Fed has the power to move markets with interest rate decisions and other measures that can affect investment capital flows. The Fed’s actions are often met with great anticipation and cause massive fluctuations in the stock market due to changes in investor sentiment. Interest rate hikes and changes in QE measures can influence investors’ expectations of future returns, therefore driving stock prices both up and down. As a result, large swings in the stock market can be seen as an indicator of how effective the Fed’s measures are perceived by investors who will buy or sell accordingly. In conclusion, it is clear that the Federal Reserve’s policies play a major role in determining market volatility.

Artificial intelligence (AI), machine learning (ML) and neural networks are powerful tools that, when properly utilized, can be a great asset to traders in their decision-making processes. AI is particularly beneficial for identifying patterns in the stock market that may not be immediately apparent from traditional analysis methods. ML offers the ability to analyze huge amounts of trade data accurately and quickly, allowing for faster and more accurate decisions. Neural networks enable traders to incorporate past experiences into making future trading decisions, which can help reduce the risk of costly mistakes. With these three tools combined, traders can make informed and confident decisions with greater probability of successful outcomes.

The bottom line is after all the bottom line.

This phrase can refer to making tough decisions that may not always guarantee public popularity. For traders, it boils down to the need to stay afloat financially and beat inflation to remain competitive in an ever-changing market.

It’s all about bringing more money by staying on the right side, of the right trend at the right time.

Dollars are being debased. Financial assets are increasing in price because the Fed is purchasing assets that no one else will.

While I have shared my opinion with you about what I see is the fundamental current economic environment, I want to be clear I never let my opinion interfere with my trading decisions.

My reality is always formed by what I see, hear, feel, and understand. I’ve come to appreciate that what I see, hear, feel, and understand is a very small universe indeed. Therefore, I use artificial intelligence, neural networks, and machine learning to guide my trading decisions.

Everybody has had horrible trades. The difference between the winners and losers in life is that the winners learned very powerful lessons from their losses.

Artificial intelligence is so powerful because it learns what doesn’t work, remembers it, and then focuses on other paths to find a solution. This is the Feedback Loop that is responsible for building the fortunes of every successful trader I know.

If you think about this question, you will begin to appreciate that AI applies mistake prevention to discover what is true and workable. Artificial Intelligence applies mistake prevention as a continual process 24 hours a day, 365 days a year towards whatever problem it is looking to solve.

That should get you excited because it is a game-changer.

Don’t sit around waiting and hoping for the Fed to pivot.

Stay informed to the highest probability analysis afforded by artificial intelligence.

Since artificial intelligence has beaten humans in Poker, Chess, Jeopardy and Go!, do you really think trading is any different?

Knowledge. Useful knowledge. And its application is what A.I. delivers.

You should find out. Join us for a FREE Live Training.

We’ll show you at least three stocks that have been identified by the A.I. that are poised for big movement… and remember, movement of any kind is an opportunity for profits!

Discover why artificial intelligence is the solution professional traders go-to for less risk, more rewards, and guaranteed peace of mind.

Intrigued? Visit with us and check out the a.i. at our Next Live Training.

Discover why artificial intelligence is the solution professional traders go-to for less risk, more rewards, and guaranteed peace of mind.

It’s not magic. It’s machine learning.

Make it count.

THERE IS A SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.IMPORTANT NOTICE!

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.