When I was first studying economics, I vividly recall wondering if I would’ve been able to recognize the significance of the Bretton-Woods Agreement in 1944 which established the U.S. Dollar as the reserve currency of the world. At the time, I would let my imagination run wild as to where I would’ve invested my money during that era of history.

The Bretton-Woods Agreement pegged world currencies to the U.S. dollar, and the dollar to gold at $35 an ounce. Fast forward to 2025 with perfect hindsight, and it’s clear that gold and U.S. stocks were the champions of investment following that historic agreement. Gold, fixed at $35 until Nixon called off the gold standard in 1971, skyrocketed to over $800 by 1980 — a staggering 2,200% increase as inflation surged. U.S. stocks mirrored this ascent, the S&P 500 climbing from about 10 points in 1944 to over 100 by the 1970s, fueled by America’s post-war economic surge.

On the flip side, fixed-income investments like U.S. Treasury bonds and cash held in weaker currencies faced the brunt of inflation and instability. Bonds issued in the ’50s, yielding just 2%, became nearly worthless in real terms by the ’70s when inflation hit 10%. Cash in countries like France and Italy depreciated significantly as their currencies floundered against the dollar until the system unraveled in ’71. Bretton Woods was indeed a monumental setup: it launched gold and stocks to incredible heights but left bonds and unstable currencies in the dust.

Now 81 years later, I am getting what I wished for as the world is experiencing Trump 2.0 and the implementation of the Mar-a-Lago Accords.

Back in November 2024, a guy named Stephen Miran wrote an important essay. He’s an economist who’s now the head of a group that gives economic advice to President Trump. His essay is called “A User’s Guide to Restructuring the Global Trading System,” and it’s all about a big idea he calls the “Mar-a-Lago Accords.” Mar-a-Lago is the name of Trump’s fancy home in Florida, so it’s like naming the idea after his house!

Imagine the world is a giant playground where countries trade stuff like toys, food, and clothes. The U.S. uses dollars to buy and sell things, and right now, the dollar is super strong — like the coolest kid on the playground who everyone wants to trade with. But Miran thinks this strong dollar makes it tough for American workers who make things, like cars or furniture, because other countries can sell their stuff here cheaper. It’s like if your toys cost $5 but someone else’s only cost $2 — everyone would buy theirs instead!

So, Miran’s big plan in the essay is to make the dollar weaker on purpose. Why? To help American workers sell more of their stuff to other countries and balance things out. He calls this plan the “Mar-a-Lago Accords” because he imagines the U.S. teaming up with other big countries — like Japan or Germany — to agree on this together, kind of like a playground pact. They’d all work to tweak their money so the dollar isn’t so strong, and everyone’s toys cost about the same.

He also has some wild ideas to make this happen, like charging other countries a fee (tariffs) for holding U.S. money or asking them to buy super long-term debt obligations (called bonds) from the U.S. instead of short-term ones. It’s like saying, “If you want to play with us, you’ve got to follow these new rules!”

The essay is a big deal because it’s a theoretical map for how Trump’s team might try to change the way the U.S. trades with the world. It’s not a done deal yet — just a bunch of ideas on paper — but it could shake things up, like changing the rules of your favorite game to make it more fair for everyone.

I’ve been pondering these ideas a lot lately because they run counter to everything I thought I knew about economics and finance. What smells off to me is that traditionally you judge the health of a nation by the strength and demand for its currency. A strong currency and high interest rates are what I always assumed defined the economic health of a nation. In the Mar-a-Lago Accords, Miran is suggesting the complete opposite.

The Mar-a-Lago Accords pursue two key tactics: lower interest rates and a weaker dollar.

Low interest rates encourage companies to borrow cheaply, fueling investment in factories and hiring — ultimately boosting economic growth and employment. On the other hand, a weaker dollar makes American products more affordable overseas, strengthening U.S. competitiveness, revitalizing domestic manufacturing, and addressing trade imbalances. Trump during his first administration was a big fan of promoting negative interest rates. Negative interest rates are when a bank charges you to keep your money instead of paying you interest — like if you put $100 in the bank and a year later, you only have $99 because they took a fee. It’s a weird trick central banks use to push people to spend or invest rather than save, hoping to kickstart the economy when it’s sluggish.

In short, Trump’s playbook revolves around reshaping economic policy to enhance America’s global economic position — rebalancing trade dynamics and fostering domestic prosperity.

The prevailing question haunting financial markets recently is whether President Trump is deliberately destabilizing the U.S. stock market. Such a notion would have seemed ludicrous prior to his presidency, given Trump’s background as a businessman who likely views market performance as a barometer of economic health and his performance, fostering expectations of a bullish market under his leadership. However, current market dynamics and policy decisions suggest that the administration might be influencing a market downturn, a scenario that contradicts prior expectations and raises profound questions about the underlying strategies at play.

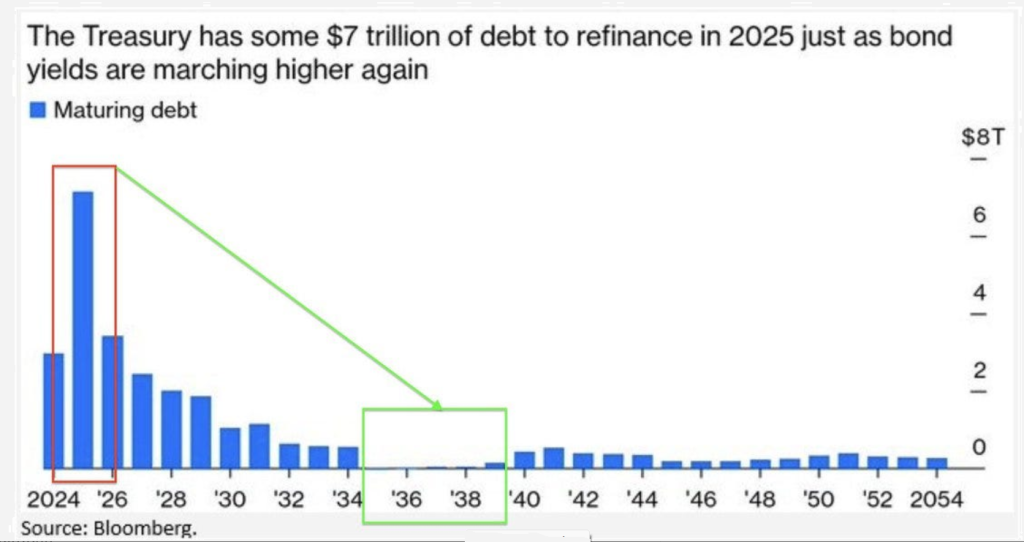

In the face of a looming $7 trillion debt payment due within the next six months, the Trump administration is strategically navigating economic levers to avoid refinancing at steep interest rates, which recently peaked at 4.8% for 10-year Treasury bonds. The administration’s tactic? Injecting market uncertainty through tariffs, which paradoxically could slow economic growth temporarily but also drive bond purchases — spurring a flight from stocks to bonds, thereby lowering yields. This counterintuitive approach seeks to pressure the Federal Reserve to reduce interest rates further, ultimately easing the fiscal burden by reducing refinancing costs. This strategy underscores a nuanced manipulation of market dynamics, challenging the traditional economic understanding that tariffs solely lead to inflation and higher long-term yields. Instead, this policy maneuver aims to recalibrate financial conditions in favor of more sustainable government debt management.

When you study this chart, you can see how debt maturities trail off after 2025. What rightfully worries traders is since bonds have been so toxic over the past 5 years, it is painfully clear that the government may be forced to run the monetary printing press and unleash another massive wave of inflation.

The Trump administration’s Mar-a-Lago Accords propose a bold shift in Treasury issuance: extending the average term from 3 years to a century. This strategic pivot aims to stabilize long-term economic planning and ensure fiscal accountability amidst rising inflation and investor hesitancy to lock in long-term funds due to fears of significant purchasing power loss. To attract investors, these 100-year bonds might need backing by robust assets like gold or Bitcoin or offer additional tax incentives. While ambitious, this plan confronts significant challenges given the recent underperformance of Treasury instruments, presenting a complex landscape for potential investors.

The Mar-a-Lago Accords are poised to whip up significant volatility in the financial markets, primarily due to their complex and multifaceted nature. These policies defy traditional economic categorization and are challenging for market participants to fully understand. As traders and investors struggle to predict the implications of these accords, we can expect heightened uncertainty and fluctuations in market prices. This complexity makes the Accords a wildcard in global finance, stirring both intrigue and instability across financial landscapes.

The U.S. is dancing on a fiscal volcano, and here’s the shocker: in February alone, for every dollar the government spent, 51 cents was borrowed money. This is a disaster in slow motion. If we keep kicking this can down the road, we’re not just risking a little market turbulence — we’re talking about the total annihilation of the dollar and the global trade system as we know it.

Now, hold onto your hats because doing nothing? That’s the fast track to catastrophe. We need a radical pivot, and maybe, just maybe, the Mar-a-Lago Accords are the wild card we need. And guess what? This isn’t just political fluff. Real changes are coming down the pipeline: tariffs, a sovereign wealth fund, reduced regulations, a strategic bitcoin reserve, negotiate tougher deals with Europe. These aren’t just plans; they’re happening.

Here’s the bottom line: billions, no, trillions of dollars are at stake here, and if these Accords pull through, it’s not just good news — it’s great news for every American. But will the markets swing our way too? That’s the trillion-dollar question.

Trump 2.0 appears to be blending elements from various schools of economic thought, which may appear contradictory to those unversed in economic principles. At its heart, the Accords propose bold changes to trade and finance, echoing mercantilist strategies by advocating for a weaker dollar to improve U.S. trade positions — reminiscent of historical tactics aimed at “winning” trade and repatriating jobs. Yet, they also incorporate modern approaches like negotiating with global powerhouses and adjusting bond policies, mixing in Supply-Side theories by cutting taxes and reducing regulations to spur business growth. This eclectic mix creates a “Neo-Mercantilist Keynesianism,” updated with a Supply-Side twist for today’s economic landscape, aiming to foster export-led growth with significant government intervention and global coordination. It’s a fusion designed to position America’s workforce at the forefront of global economics, portraying an aggressive yet calculated strategy to dominate the economic playground.

Picture this: President Trump declares, “Hey, no taxes on lemonade stands this year!” Armed with that extra cash, investors and businesspeople would likely upgrade to a top-notch juicer, bring your cousin on board, and start selling lemonade far and wide. Proponents of Supply-Side Economics would point to this as a sign of booming economic activity.

Essentially, Supply-Side Economics turbocharges producers, aiming to sweeten life for everyone by ramping up production. It’s all about empowering the creators, making them the hero of the economic narrative.

We are witnessing what could be described as the Age of Economic Turbulence, with each day bringing a new policy announcement or significant action from President Trump and his administration.

“Trump Pushes for Weaker Dollar to Boost American Jobs!”

“Interest Rates Slashed—Borrowing Money Is Super Cheap Now!”

“Tariffs Hit China Hard—Trump Says, ‘Buy American!’”

“Stock Market Soars as Trump Bets on Oil and Gas!”

“DOGE Team Cuts Government Spending—Big Savings or Big Trouble?”

“Trump Unveils Mar-a-Lago Accords to Shake Up Global Trade!”

“Factories Cheer as Trump Dumps Green Energy Rules!”

“Gold Prices Jump as Dollar Weakens—Trump Says It’s Fine!”

“Trump Pressures Fed: ‘Keep Rates Low or Else!’”

“Trade Deficit Shrinks—Trump Claims Victory Over Imports!”

Plus, President Trump has signed 73 new Executive orders. The purpose of the numerous executive orders signed by President Trump is to swiftly implement key aspects of his policy agenda, specifically targeting economic, immigration, and regulatory changes. These orders aim to reshape or reverse prior administrations’ policies quickly without needing to pass through the slower legislative process, effectively setting a new direction for the administration’s priorities.

This approach, characterized by rapid changes and bold moves, has polarized opinion. Critics argue that such unpredictability may harm the U.S. economy and diminish its global standing. On the other hand, supporters commend the President for delivering on his campaign promises, advocating for a significant reduction in bureaucracy, an end to government waste, and a strong America First agenda that aims to reverse decades of globalist policies.

Last year’s financial narrative was dominated by President Trump’s vocal criticisms of Federal Reserve Chair Jerome Powell for not cutting interest rates. With Powell’s steadfast resistance to this pressure, Trump, alongside his advisor and Treasury Secretary, Scott Bessent, appears to be taking a more aggressive approach. They are seemingly driving down asset prices, an audacious strategy designed to compel the Federal Reserve into lowering interest rates. The standoff between monetary policy and executive will is a high-stakes game of financial chicken, and it’s unclear who will blink first.

The Mar-a-Lago Accords challenge traditional economic categorization, blending elements from various schools of thought, which may appear contradictory to those unversed in economic principles. At its heart, the Accords propose bold changes to trade and finance, echoing mercantilist strategies by advocating for a weaker dollar to improve U.S. trade positions — reminiscent of historical tactics aimed at “winning” trade and repatriating jobs. Yet, they also incorporate modern approaches like negotiating with global powerhouses and adjusting bond policies, mixing in Supply-Side theories by cutting taxes and reducing regulations to spur business growth. This eclectic mix creates a “Neo-Mercantilist Keynesianism,” updated with a Supply-Side twist for today’s economic landscape, aiming to foster export-led growth with significant government intervention and global coordination. It’s a fusion designed to position America’s workforce at the forefront of global economics, portraying an aggressive yet calculated strategy to dominate the economic playground.

In a strategic pivot, the Federal Reserve is moderating its approach from quantitative tightening (QT) to a stance more reminiscent of quantitative easing (QE). Quantitative tightening, which has been in effect since 2022 to mitigate post-pandemic inflation, involved the Fed reducing its holdings of Treasury securities and mortgage-backed securities to temper an overheated economy. However, starting in April, the Fed will significantly decrease its monthly reduction of Treasury securities from $25 billion to $5 billion, effectively easing the monetary contraction.

This adjustment is likely to lower borrowing costs, reflected in the crucial 10-year Treasury rate, a development welcomed by President Trump as it stimulates economic activity and could rejuvenate sectors like housing and automobiles. While this is not a full return to QE — where the Fed would aggressively purchase assets to inject liquidity — it represents a substantial softening of monetary policy. The shift is poised to lower Treasury rates and could trigger a robust stock market response if economic conditions remain favorable, though risks remain if the economy encounters turbulence.

During Trump’s first term (2017-2021), the 10-year Treasury bounced between 0.5% and 3%. Trump wants and needs significantly lower rates to effectively implement his program. We would need interest rates to fall 150 basis points further just for them to be where they were at the highest point of the Trump 1.0 administration.

The current economic strategies unfurling under the Trump administration do not necessarily resonate as universally sound, but they certainly underscore a bold reimagining of fiscal policy. The government is initiating severe cuts to public sector employment and key social programs such as Medicare, SNAP food assistance, and housing subsidies. These austerity measures are set to recalibrate within the next few months, paradoxically paired with a vigorous boost to supply-side stimulus aimed at revitalizing private industry. This includes substantial corporate tax reductions, a significant scaling back of IRS and financial oversight, and aggressive deregulation to enhance corporate profitability — all while promoting expansive oil drilling.

The strategy posits that while demand-side policies might kick in rapidly, the supply-side effects will lag, potentially leading to cyclical deflation. The administration’s response, it seems, will be a quick pivot from quantitative tightening back to quantitative easing, aiming to inject liquidity back into the economy at a crucial juncture.

According to the Fed, the latest economic forecasts paint a bleaker picture than previous assessments, suggesting an uptick in unemployment rates to 4.4% by year’s end, a rise in core PCE inflation to 2.8%, and a slowdown in GDP growth to 1.7%, marking a downgrade from earlier predictions made in December. Despite this gloomier outlook, the Federal Reserve maintains its earlier stance on monetary policy, signaling an intention to implement two rate cuts over the course of the year. This approach suggests a continued strategy to counteract slowing growth and rising inflation, aligning with their consistent efforts to stabilize the economy.

This complex tapestry of policy adjustments is spearheaded with a clear intent to execute, regardless of external opinions or potential backlash. The overarching outcome of such drastic changes is a profound level of uncertainty in economic forecasts and market stability. For investors and savers, the key takeaway in these turbulent times is the acute need to safeguard personal financial portfolios as the landscape shifts unpredictably. We are indeed poised for a bumpy economic journey ahead.

The issue that I continue to wrestle with is if the dollar is going to get weaker, and this is government policy, where should I put my money?

How is this different from currency debasement?

Let’s face it, weakening the currency might seem like a neat trick to give the illusion of prosperity — suddenly, everything priced in that currency, from groceries to gas, starts to cost more. Politicians might point to rising prices and call it growth, but ask yourself this: What kind of real prosperity is it when the price of everyday items like eggs, cheesecake and insurance outpaces the growth stock market? That’s not growth; that’s pain where it hurts, in your daily budget, making it impossible to save.

To understand the dark side of currency debasement all you need to do is look at data from any country that has had serious bouts of inflation. Their stock market grew exponentially during the crisis. Check Venezuela, Zimbabwe or Turkey.

- Zimbabwe: Currency lost trillions of percent value; stocks up millions of percent in ZWD, but flat in USD.

- Venezuela: Currency lost 99.9999% value; stocks up 20,000%+ in VEF/VES but crashed in USD.

- Turkey: Currency lost 80% value; stocks up 5,400% in TRY but flat in USD.

In economics and finance the golden rule is understanding what you are measuring as well as how you are valuing something.

My biggest issue with the Mar-a-Lago Accords is the apparent contradiction within the policies. Let me get this straight, you’re reducing the value of the currency that you are obligating me to trade in, and you are telling me this is good for me? How do you build long term wealth in a currency that is perpetually debased?

It’s like you’re diligently building a grand LEGO tower, but each night, someone secretly replaces the unused bricks with slightly smaller ones. Before you know it, your once-sturdy tower is shaky and diminished. That’s a perfect metaphor for trying to amass wealth with a currency that’s losing its punch. Imagine a dollar today could get you a whole candy bar, but tomorrow, it barely buys half a candy bar.

Even if your wallet grows fatter with more dollars, each one buys less and less, leaving you running harder on a financial treadmill that’s picking up speed. You’re putting in the effort, but your progress is illusory. How can anyone expect to build real wealth when the value of their currency is melting away like this? It feels like you’re playing a game where the rules are constantly changing — and not in your favor.

Building wealth with a currency that’s always being debased is like your boss cutting your pay by 25% per hour — say from $10 to $7.50 — just because he feels like it. Then, to “make up for it,” he gives you 6 extra hours of work a week, so you’re slinging pizzas longer, and less money. Sure, you’re getting more hours, but your paycheck is smaller and what you earn is worth less. You’re busting your butt, sweating over the oven, but your dreams keeps slipping further away because the money’s shrinking faster than you can stack it. How’s that supposed to help you build real wealth when you’re stuck running harder just to stay broke?

The Mar-a-Lago Accords are likely being implemented. As a trader and investor, it is imperative that you understand the opportunities and risks involved. When the government is telling you that they are going to push the dollar lower, it would be foolish not to believe them. What’s at stake? The Mar-a-Lago a strategic gambit aiming to overturn the global financial landscape, shatter the old norms, and position the U.S. atop the global hierarchy once again — whether you admire him or despise him, Trump is swinging for the fences, and the globe is watching, breath bated, for the outcome.

When we study the performance of different markets it’s clear that fear is in the air.

Over the past year Gold is up over 40%.

Bitcoin is up 24% over the same time frame.

Meanwhile, the S&P 500 is UP only 8.5%.

But let’s zero in on the here and now. We’re navigating through a new economic era where traditional financial tools aren’t just failing to deliver; they’re planting the seeds of future economic upheavals. The data paints a grim picture: sure, we’re outperforming many other nations, but that’s hardly a badge of honor in this context. Despite the Federal Reserve’s aggressive rate cuts, inflation remains stubbornly high, economic growth is lukewarm at best, and wages aren’t keeping up with living costs. This economic quagmire won’t be solved with more rate cuts.

Since the 2008 crisis, what we’ve seen isn’t traditional inflation but rather rampant inflation of asset prices. In 2024 alone, despite the Fed slashing rates by a full percentage point, the market reacted not with enthusiasm but with a cold shoulder, evidenced by the steepest plunge in the S&P 500 since the 2020 turmoil. This wasn’t a mere correction; this was the market outright defying the Fed. It’s clear that these rate cuts are seen as mere band-aids on deeper economic fractures.

Here’s where it gets real: the disconnect between the Fed’s moves and the market’s reactions is stark and widening. Markets now anticipate the Fed’s moves so much that they adjust in advance, lessening the impact when the rate cuts do occur. Moreover, faith in the Fed’s ability to guide the economy solely through rate manipulation is waning. The old playbook of slashing rates to spur the economy is being replaced by a growing concern over endless debt cycles and a weakening dollar.

In this era of critical observation, the relevance of the Federal Reserve’s traditional mandate — to manage the economy through interest rates — is being questioned and challenged. It’s an antiquated strategy in a world where such mechanisms no longer wield their intended power. This raises a powerful argument for embracing a true free market system, where interest rates are determined by market forces of supply and demand, not the heavy hand of a central bank.

I wish the new administration in charge could turn this mess into a wild success. But let’s get real — Washington D.C. is a swamp of problems that aren’t going away without some real smarts thrown at them. Until I see a plan that doesn’t just stack more debt on our already colossal pile, count me skeptical and not holding my breath for politicians to fix deep economic wounds.

Now, shifting gears to you, the trader hitting wall after wall — everyone starts with big dreams of financial freedom, but the cruel market often sends folks packing with their tails between their legs. It’s not just about picking stocks; it’s about surviving in a minefield where risk is your constant shadow. Day in, day out, you’re making calls that could skyrocket your success or sink you into misery.

Today Trump 2.0 is telling you loud and clear that the plan for the future is to debase the currency further and faster. So, you have to anticipate a hurdle rate of at least 8% per year just to break even and maintain your purchasing power moving forward.

Are you prepared for these new rules of engagement from the Mar-a-Lago Accords?

Do you have the ability to find investments and trades that can outpace this level of currency deterioration?

Trading isn’t always a stroll in the park. It can be an emotional warzone. Fear, doubt, and panic join every dip in the market, ready to dance on your decisions. And it’s not just emotions messing with your head; the barrage of endless data and complex charts can make anyone’s brain spin. It’s a battlefield, and if your emotions are calling the shots, you’re in trouble.

But what if there was a way to slice through the chaos and clutter? Enter stage right: Predictive artificial intelligence trading software, your new ace in the hole. This isn’t about some robotic overlord; it’s about harnessing tech to make smarter, data-backed trading decisions. A.I. doesn’t panic; it processes. It’s tirelessly analyzing trends, data, spotting opportunities with the kind of precision that only comes from cold, hard algorithms.

With A.I. from VantagePoint, you’re not just trading — you’re dominating. This tech isn’t about playing catch-up; it’s about setting the pace. Armed with insights from A.I., your trades are based on solid data, not gut feelings or hunches. Imagine having a supercomputer sidekick that helps you dodge pitfalls and snatch opportunities the second they arise.

Ready to transform your trading game?

Dive into our online trading master class and Learn How to Trade with A.I. This is your golden ticket to learning from the pros, seeing A.I. in action, and understanding how to leverage it for consistent success in trading.

This is your chance to learn from the experts, see AI in action, and understand how you can apply it to achieve consistent trading success.

Hit up the link, sign up for the A.I. trading masterclass, and jump into the future of A.I.-driven trading.

Let’s Be Careful Out There!

It’s not magic.

It’s machine learning.

THERE IS A SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.IMPORTANT NOTICE!

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.