In the high-stakes world of trading, where fortunes can pivot on the dime of market fluctuations, money management emerges not merely as a strategy, but as the cornerstone of survival and success. Any seasoned gambler knows the folly in betting the entirety of one’s bankroll on a single, precarious roll of the dice. A negative outcome wouldn’t just dent the wallet, it would obliterate one’s ability to play the game at all. Similarly in trading, the peril of placing too much capital in one position exposes traders to the harsh classroom of market realities. Most traders, driven by the initial thrill of potential gains, often overlook the sobering necessity of risk management and precise position sizing, only to embrace it after the market delivers its expensive lessons in loss. This fundamental truth underscores that in the turbulent dance of the markets, preserving capital through meticulous money management is not just prudent — it’s paramount.

Nowhere is this better illustrated than in the insurance market. Lloyd’s of London, one of the world’s leading insurance and reinsurance markets, has a rich history that dates back to the 17th century. Its foundation is tied to Edward Lloyd’s coffee house, opened around 1686 on Tower Street in London. The establishment became a popular gathering place for ship captains, merchants, and ship owners, leading to the informal exchange of shipping news and eventually the underwriting of maritime ventures.

The tremendous mystery surrounding the insurance business largely stems from its complex nature and the intangible aspect of what it offers — protection against potential future losses. While many people regularly purchase insurance, few understand the intricacies of how these companies operate and manage risk. Lloyd’s, as a conglomerate, exemplifies the profound profitability that can come from assuming risk from consumers. This practice has proven to be extremely lucrative, as effectively managing this risk translates directly into financial gain.

From its early days, the members, or “Names,” of Lloyd’s took on unlimited liability; they were personally and fully responsible for the risks they underwrote. This unlimited liability meant that there was potential for immense profit but also for catastrophic losses. Today, while the structure of Lloyd’s has evolved, with corporate members now holding a significant share of the risk, the principle of shared risk remains.

At the venerable Lloyd’s of London, the participants engage through syndicates, those uniquely structured teams that underwrite the vast and varied world of insurance. Within these syndicates, liability is meticulously confined to the extent of resources pledged by the members themselves. It’s a business that spans the spectrum of risk, from routine to the utterly extraordinary.

Consider the array of transactions handled: marine insurance, securing the vast commerce of the seas by covering ships and their cargoes; property insurance, a bulwark protecting the tangible investments in real estate; casualty and liability insurance, shielding against the financial fallout of legal entanglements.

At Lloyd’s of London, the insuring of the extraordinary is not just business as usual; it’s an art form that weaves risk into reward with surgical precision. This prestigious institution is famed for underwriting some of the most unusual and extravagant insurance policies the world has ever seen, like those covering celebrity body parts. Take, for instance, the iconic legs of Marlene Dietrich, insured for a million dollars each in the 1940s, or Bruce Springsteen’s voice, valued at $6 million during the 1980s. These policies underscore not just the high stakes involved but also the unique risks associated with insuring such rarefied assets.

Members of Lloyd’s syndicates engage in these ventures by taking on a slice of the risk, and in exchange, they garner a corresponding share of the premiums. This structure allows them to participate in premium opportunities that the ordinary insurance market rarely touches. It’s a gamble, sure, but one meticulously calculated. Now, consider the parallel in the world of finance, particularly in the selling of Put Options. Here too, traders essentially insure the value of someone else’s portfolio. By selling a put option, they agree to buy stocks at a predetermined price, should the markets falter, much like a syndicate member might pay out on an insured celebrity’s unforeseen mishap. In return, they receive premiums upfront — payments for bearing the risk that others are unwilling or unable to shoulder themselves.

This dynamic of premium for risk ties the methods of Lloyd’s syndicates to Put Options traders. Both are in the business of pricing risk and profiting from the premiums paid by those who seek to hedge against potential losses. Whether it’s the physical assets of a superstar or the stock values in an investor’s portfolio, the principle remains the same: accept the risk, manage it wisely, and the premiums collected become a source of steady income. It’s a fascinating confluence of finance and insurance, each playing out their high-stakes drama against the backdrop of market forces and human endeavors.

The threat of loss weaves the very fabric of the insurance industry. In its simplest form, insurance exists because of the universal aversion to loss — whether that’s from fire, flood, or the myriad other misfortunes that can befall individuals and businesses. Yet, this concept of mitigating risk extends beyond mere physical or tangible assets. It also encompasses the financial markets, particularly in the pricing of assets. Here, price insurance manifests through the options market, a critical tool for investors seeking to hedge against price volatility or to speculate on future movements.

Many traders are well-versed in the buying of Options. This practice allows them to manage risk by paying a premium to secure the right to buy or sell an asset at a predetermined price, thus capping potential losses while maintaining the possibility of unlimited gains. Yet, despite its critical role, there exists a palpable squeamishness among many about stepping into the role of an option seller. This hesitation stems from the potential for large, albeit unlikely, losses if the market moves significantly against the position.

However, what often eludes the typical investor is the perspective that selling options, much like selling price insurance, can indeed be a remarkably profitable venture. This is where the philosophy diverges significantly. The greatest money managers and traders, the Buffetts, the Dalios, the Soros and their ilk, understand that selling Options is akin to assuming the role of the insurer rather than the insured. It’s about collecting premium payments, and in a well-managed portfolio, these premiums add up to a steady, consistent income stream.

Selling Options effectively requires a nuanced understanding of market dynamics, risk assessment, and rigorous discipline. The best in the business appreciates that, like selling any form of insurance, there is a calculated risk, but when performed judiciously, the probabilities are often in their favor. By writing Options, traders essentially bet on the stability or minor fluctuations within a market or stock, as opposed to dramatic shifts. They leverage statistical and historical data, crafting strategies that benefit from the erosion of time value in options — a concept known as “theta decay.” This approach capitalizes on the inevitable decline in option prices as the expiration date approaches, provided the underlying asset remains relatively stable.

In essence, the business of selling price insurance through Options is not for the faint of heart nor the uninformed. It demands a deep market understanding, a robust risk management framework, and, above all, an investor temperament that is both patient and disciplined. Yet for those who master it, selling Options is more than a strategy; it’s a cornerstone of financial empire building, underpinning some of the most successful investment careers in the world.

Selling Options in the financial markets shares a striking resemblance to the business model employed by casinos. Both rely on a deep understanding of probabilities and risk management to ensure long-term profitability.

In the context of a casino, the house meticulously designs each game to have a built-in statistical advantage, often referred to as the “house edge.” This advantage ensures that over many games, the casino will make a profit because the odds are slightly tipped in its favor. For instance, in the game of roulette, the presence of zero or double zero on the wheel creates a scenario where the payouts on a bet are slightly less than the odds of winning that bet. The casino doesn’t need to win every wager; it simply needs to keep playing the game over and over, and the law of large numbers assures it of a profit over time.

Similarly, when traders sell Options, they are essentially adopting the role of the casino by leveraging the probabilities inherent in options pricing. Options sellers collect premiums upfront from the buyers of the options. These premiums represent the price the buyers pay for having the right, but not the obligation, to execute the option at a future date. The sellers of options, like the casino, know that a significant portion of options expire worthless, allowing the sellers to keep the entire premium.

The key to successful Options selling, much like operating a profitable casino, lies in understanding and managing the risks. Options sellers use various strategies to mitigate risk, such as hedging positions or choosing options with a favorable risk-reward ratio based on implied volatility and other market factors. This risk management ensures that they can endure the instances when the market moves against them, much like a casino absorbs the occasional big payout to a winner.

In both cases, the operator — whether a casino or an Options seller — relies on statistical edges and risk management to maintain profitability. They both accept that they will not win every transaction but trust that their advantage in probabilities will yield a profit in the long run. Thus, the essence of their business models revolves around creating and managing activities where the odds are tilted in their favor, leveraging the law of large numbers to achieve consistent returns.

Let me explain with an example that will drive this point home.

At any given time, in every market there are bulls and bears. There is always a huge variance of opinion over where the price of an asset will be in the future.

Within this variance of opinion is where trade occurs.

Bulls are concerned about the threat of loss.

Bears are concerned about the threat of loss.

This is how the options market comes into existence and offers traders the opportunity to “insure their portfolios” against a catastrophic loss by purchasing Options.

Every Option is a time sensitive instrument which guarantees the buyer the right but not the obligation to buy or sell the underlying asset at an agreed upon price in exchange for a premium payment they receive now.

The creator, or seller of the Option has an obligation to either make or take delivery of the underlying asset at the agreed upon price. For this obligation they receive a premium payment.

The plain simple truth is that most Options contracts expire worthless. Whenever this occurs it essentially means that the option creator, the seller, received the premium payment and was never exercised to fulfill the obligations of his contract.

This reality often escapes many traders.

I think about this regularly whenever I pay my insurance premiums.

Alright, let’s talk brass tacks about selling Put Options. Selling puts is like being the guy at the poker table who doesn’t play his cards, but bets on everyone else’s hands. You’re selling someone the right to sell you their stock at a predetermined price before a set date. Now, why would anyone want that? Because they’re scared the market’s going to tank and they want an out. So, you take their fear, stamp a price tag on it, and pocket the premium.

But here’s where it gets spicy. The rewards? They’re sweet. Each time you sell a put, you collect cash up front. It’s like laying down a welcome mat that says “Payday.” If the stock stays flat, rises, or doesn’t drop below the strike by expiration, you’re golden. You keep the full premium, no stocks change hands, and you walk away grinning.

The most you can make when you sell a put option is the premium you collect. So, this strategy is not for the timid. Put sellers are very selective. They look for unjustified FEAR and then play the odds accordingly.

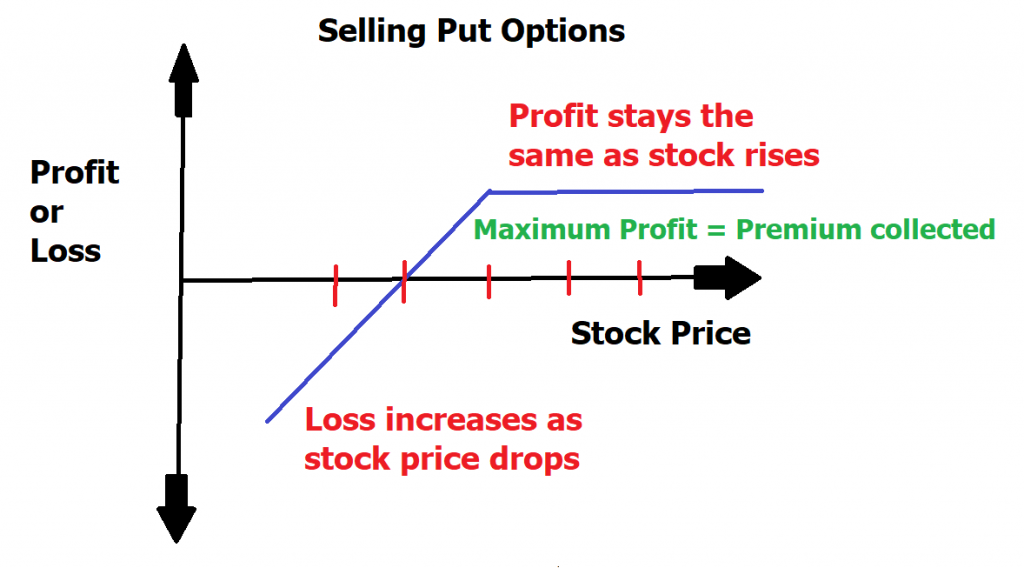

Here is the risk reward profile of Selling Puts

The risks of selling a put can be the entire price of the asset. This theoretically can occur because the asset can go to zero.

Let me share a conceptual example of this so that the idea strikes home.

Over the past few months Bitcoin ($BTC) has rallied 50%. Believers think it can go to the moon. Bears on the other hand think it is a scam and will go to zero.

Here is how a put option seller might approach the bitcoin market based upon current conditions.

Sell 1 December 2025 $30,000 Bitcoin Put for $1,200.

Let’s review all the components of this trade for purposes of creating clarity.

The December Bitcoin put options are set to expire on December 27, 2025.

The Put option seller is agreeing to buy bitcoin at a price of $30,000 in exchange for this obligation they are receiving $1200 today.

The breakeven point for the Put option seller is the $30,000 strike price less the $1200 premium received. In essence, what we can conclude from this perspective is that at any price over $28,800 at the December Expiration the Put Option seller will be profitable.

This is not an exciting strategy. But you can see how the probabilities clearly favor the Put Option seller.

Let’s look at something closer to the current bitcoin market price.

Sell 1 December 2025 $90,000 Bitcoin Put for $16,065.

This option expires December 27, 2025.

It obligates the Option seller to buy bitcoin at $90,000. In exchange for this obligation the put option seller receives a premium payment of $16,065 NOW.

The breakeven price for the Put Option seller is the strike price of $90,000 less the premium payment of $16,065. We can conclude that at expiration at any price over $73,935 the Put Option seller will be profitable.

For a Bitcoin bull who liked Bitcoin at $90,000, you can imagine how thrilled they would be to be exercised a position with a breakeven price of $73,935.

This is why all the top money managers make Put Options Selling a part of their money management.

Once again it is not very sexy. But it is very calculated and extremely strategic.

What a Put Option seller will do in every instance is place a Good-Till-Cancelled Stop order at their breakeven price in the market to protect themselves against a cataclysmic decline. That way should prices fall, a lot their obligation of owning Bitcoin will be offset by their Good-Till-Cancelled sell order.

The risks? They can bite hard. If the market dives and the stocks plummet below that strike price, you’re on the hook to buy them at that agreed-upon strike price, which now looks like a skyscraper in a sinkhole. This means you could be forced to buy at a hefty loss or hold onto stocks worth less than what you paid, chewing into your capital like a starved rat. And if you’re not judicious with your position sizing or money management, one bad roll can wipe out a string of those nice little premium paydays.

So, selling Put Options isn’t for the faint of heart. It’s a game of probabilities, knowledge, and a knack for sniffing out just how jittery the market is. Play it smart, manage your risks like a hawk, and the rewards can be consistently lucrative. But remember, in this high-stakes game, always be prepared to pay the piper if the market decides to sing a dirge.

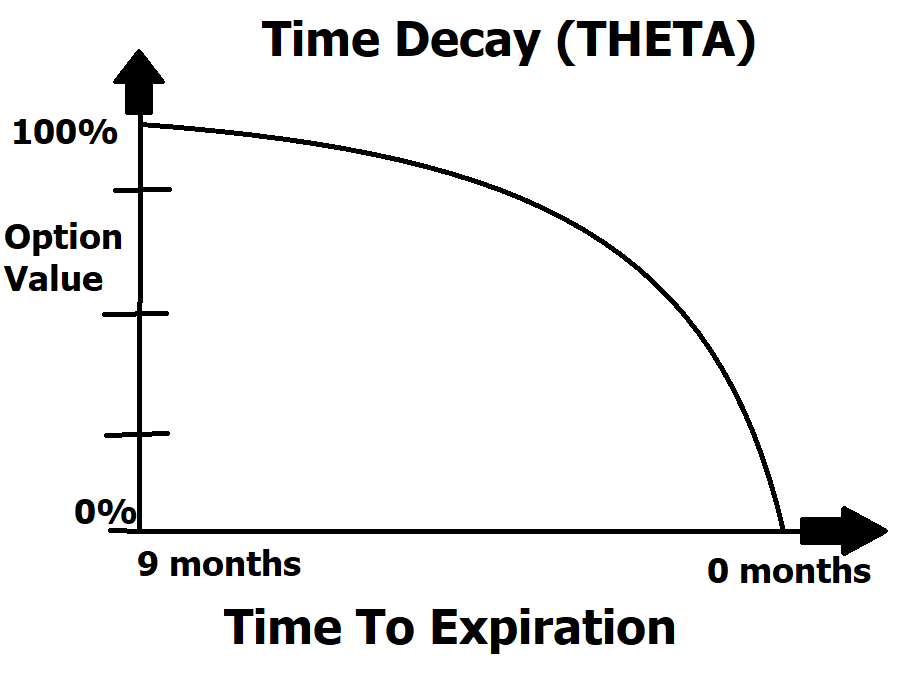

When you’re playing the game of options in the financial markets, there’s one thing you gotta keep your eyes glued to: time. Why? Because, time and that wild beast called volatility are what make your options tick. Think about it: the more time an option has to cook before it hits its expiration, the pricier it’s going to be.

Now, let’s talk about volatility. This is where the market dances like a disco on steroids. The more an asset jumps around, the more traders sweat about what they’re going to do next. And what does that mean for you? Higher prices, baby, because risk is the name of the game, and uncertainty means people are willing to pay more to sleep at night.

But here’s the kicker, the real juice: we know when the party ends. We’ve got the expiration date, and that’s gold. This little gem lets us play fortune teller with how much these options will deflate each week. And let me tell you, there’s nothing sweeter than watching the value of an Option melt away like ice cream on a hot sidewalk, especially when you’re the one collecting the premiums. That’s why the smart cookies, the real sharpshooters of trading, zero in on those options expiring in the next 30 days. They know that the closer to D-day, the faster the time decay, the faster their bank accounts puff up. It’s like picking up cash in the wind — easy work if you can get it.

What makes this tactic extremely exciting is that whenever you sell a Put Option you can be completely wrong in terms of price movement and still make money. The price of an asset can fall a lot, but as long as it doesn’t fall past your breakeven price before the expiration date your option will expire worthless.

In today’s complex financial landscape, many stocks feature Options that expire on a weekly basis. Grasping the mechanics of this strategy is essential for any investor aiming to consistently tip the scales in their favor, while also generating a steady stream of income for their portfolio. This understanding isn’t just advantageous; it’s imperative for those who intend to navigate the turbulent waters of the options market with skill. As these Options bring both opportunities and challenges weekly, a thorough comprehension not only equips investors to capitalize on potential gains but also to fortify their investments against unforeseen market shifts.

In the periods of bull markets, selling Put Options is astonishingly simple. When the market trends upwards, optimism fuels the environment, making this approach virtually child’s play.

But beware the dark shadows of a bear market! Here, selling Put Options transforms into a dangerously high-stakes gamble. The downward spiral of stock prices can turn what seems like a clever strategy into a devastating financial blunder. In these treacherous times, the method that once seemed foolproof can quickly become a pitfall, swallowing profits whole. Proceed with the utmost caution, or better yet, steer clear until the storm passes.

This is why trend analysis through artificial intelligence is so vital.

Great trading isn’t about striking gold when you’re right — it’s about not sinking when you’re wrong. Discover the art of selling Options and collecting premiums; a method so savvy, you can afford to be wrong and still watch your profits grow.

Imagine a tool so adept at learning from its failures that it never makes the same mistake twice. That’s the power of artificial intelligence. It tirelessly works around the clock, every day of the year, perfecting its strategies and safeguarding your trades from common pitfalls.

Now picture yourself mastering the craft of selling Put Options. With minimal risk and supreme money management, you position yourself ahead of the pack, beautifully outpacing the herd before they even catch wind of opportunity.

But there’s more. The latest in A.I., machine learning, and neural networks isn’t just an advantage; it’s essential armor for your portfolio. Why settle for the old ways when A.I. offers groundbreaking solutions that minimize risk while maximizing rewards?

Join our next live training to see the revolutionary A.I. in action.

This isn’t just smart trading. It’s trading transformed by machine learning.

Ready to make each move count?

Explore how A.I. can redefine your trading strategy and keep you ahead of the curve.

It’s not magic — it’s machine learning, and it’s within your reach.

Visit with us and check out the A.I. at our Next FREE Live Training.

THERE IS A SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.IMPORTANT NOTICE!

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.