In the twilight of the 1980s, my journey as a trader and investor began, an era freshly scarred by rampant inflation. This economic turmoil compelled Fed Chairman Paul Volcker to push interest rates to a staggering 21%, a desperate bid to recork the inflation genie’s bottle. That episode etched a profound realization in my mind: the daunting challenge of safeguarding savings against a government’s relentless printing press, which can dilute personal wealth on a whim. This harsh financial truth has haunted me over the past four decades.

During this period, I’ve witnessed the price levels of most goods and services soar by 600%. Meanwhile, I’ve endured endless assurances from politicians and monetary authorities, proclaiming the economy’s strength and resilience. Yet, the reality I’ve observed tells a different story — one lurching from one financial crisis to another, all while sidestepping the core issue: our monetary system is fundamentally flawed. This cycle of crisis and misguided reassurance underscores the undeniable truth that the turmoil we face stems from a broken monetary foundation.

Our so-called monetary masters have cooked up a theory that’s as dangerous as it is seductive: they claim you can extinguish a raging debt inferno by throwing more debt on the fire. Flip on the news, and you’ll catch their smooth-talking heads selling this snake oil with the finesse of old-school carnival barkers. They’re convincing. But here’s the gritty question they don’t want you to ask — why has socking away a few bucks become an exercise in futility?

Stash your cash in a bank or tuck it under your mattress, and you’re signing up for a guaranteed loss in purchasing power. It’s a rigged game. According to the high priests of high finance, every last one of us is now a speculator, whether we signed up for it or not. As you scramble to shield your hard-earned money from the silent thief of inflation, you’re herded into the gladiatorial arenas of the stock market, forced to chase assets just to stay ahead of the real rate of inflation.

This, according to our esteemed economic leaders, is what a strong and resilient economy looks like. If that’s their definition, we’re all in deeper trouble than we thought.

The challenge I have as a trader and investor is that regardless how I analyze the tariff concerns, I am very skeptical of the Trump administration’s ability to correct all of the structural excesses that continue to destroy the purchasing power of the US dollar. Trump and his cabinet all believe in a weaker US dollar and negative interest rates. Both ideas fly in the face of common sense when it comes to defining the health of a currency and country.

What I’m about to tell you might shock you. As of this very moment, while I’m banging out this article, a whopping 493 stocks in the S&P 500 haven’t budged an inch in the first quarter. That’s right, flat as a pancake, despite soaring to dizzying heights in 2024 and all the doom and gloom headlines we’re seeing in 2025. And if you peek at the Bloomberg US Large Cap Index, minus the big-shot Magnificent Seven, it’s the same old story: flat year-to-date.

So, what’s keeping investors up at night? Two things: slashing spending and the terror of tariffs. But here’s the kicker: cutting back on government spending is crucial. It’s the surgeon’s scalpel we need to trim down that bloated inflation and hack away at our monstrous $2 trillion deficit. Last year, government spending ballooned by 10%, a figure so outlandish it’s practically a scene-stealer, dragging our GDP growth down to the worst it’s been since the Great Depression, once you factor in the debt pileup.

Now, let’s talk tariffs because it seems the whole globe is in a tizzy over them. Most investors are snoozing through the real story, blissfully ignorant of the gigantic trade walls the European Union and China have been erecting for years. And while they’re at it, they’re cool with the tariffs other countries slap on us but raise a stink when we return the favor.

But here’s the real scoop: Tariffs aren’t the bogeyman that’s going to inflate your dollar into oblivion. Nope. They’re not cranking up the money supply or making cash change hands faster. What they are is a rough-and-tumble tool to square things up, to shrink the massive trade deficit we’ve got because Uncle Sam’s been too nice, letting everyone else play tough while we play fair.

I’ve got to hand it to the Trump administration; they’re really trying to steer the ship in the right direction. It’s not the tariffs that keep me up at night. Trump’s trying to hammer out better deals, and I’m all for giving credit where it’s due. But here’s what really grinds my gears: I believe America has become a fiscal ZOMBIE nation. No kidding around here. We’re borrowing 51 cents on every dollar just to pay back old debts. It’s a freak show of financial mismanagement that’s turning our economy into a walking dead. And until we tackle this structural mess head-on, our dollar’s going to keep losing muscle faster than a steroid-pumped sprinter.

Now, some folks get jittery thinking tariffs, spending cuts, and inflation fears mean a tighter belt for everyone — less money circulating, fewer sweet deals from the Fed. But here’s the thing: a bit of short-term sting sets us up for long-term success. We’re talking about reigniting real wages, beefing up our financial muscles, and getting the economic engine purring again.

Remember, the U.S. economy is a beast. With the right moves — spending cuts, tax relief, and fair-trade deals — it’s not just surviving; it’s set to thrive. Pain today for gain tomorrow, folks. That’s the long and short of it.

But let’s address the ZOMBIES in the economy.

Zombification in the financial world is a phenomenon where markets, companies, and even entire countries fall into a state of economic limbo, kept artificially alive by the relentless infusion of cheap debt. In the accounting world, this translates to balance sheets that become more fiction than fact, filled with assets whose values are uncertain and liabilities that keep piling up.

Companies turn into zombies when they earn just enough to continue operating but not enough to meaningfully pay off their debts. They are the walking dead of the corporate world — operating, yes, but with no real prospect of recovery. This state is made possible and perpetuated by the unprecedented ease of accessing debt, thanks to central banks’ policies that keep interest rates low to encourage borrowing. It’s a seductive trap: debt is cheap, so why not borrow it? But this leads to bloated corporate structures that resist innovation and instead focus on survival.

For markets, zombification means that traditional signals such as price discovery become distorted. When money is cheap, investors chase yields without regard to the underlying economic realities, leading to inflated asset prices and bubbles that don’t reflect economic fundamentals. Market dynamics shift from reflecting economic health to a game of musical chairs, where nobody wants to be caught standing when the music stops — the music in this case being the easy monetary policies.

At the national level, countries can become zombie states when they rely on continuous borrowing to fund their expenditures instead of fostering genuine economic growth. This reliance on debt leads to a cycle of borrowing and rolling over old debt with new debt, never truly addressing underlying economic issues. Like zombie firms, zombie countries are trapped in a cycle of stagnation, unable to make significant progress in reducing debt or generating real economic recovery.

In essence, the zombification process is facilitated by the modern financial system’s capacity for debt creation. It turns potentially vibrant economies into slow-moving giants unable to respond agilely to economic changes. The irony is thick: what is meant to be a mechanism for growth becomes a shackle, chaining entities to a cycle of dependency that can be incredibly difficult to break. This debt-driven survival is normalized in our financial culture, heralding a dangerous shift in how economic success is measured and achieved.

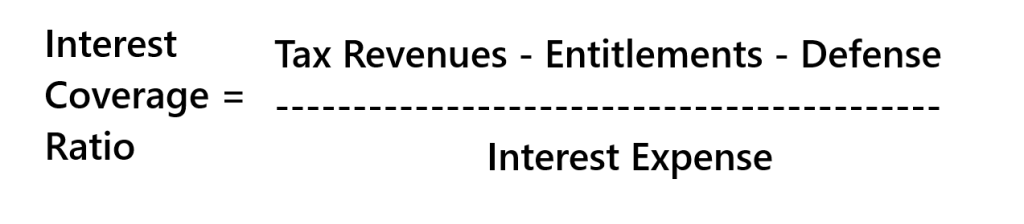

Here’s the formula that accountants have used for generations to define ZOMBIES.

Now, let’s toss in the latest numbers like a seasoned card dealer flipping a royal flush:

– Tax Revenues: The big pot, the total cash coming into Uncle Sam’s coffers. For FY 2025, this is projected at around $5 trillion.

– Entitlements: These are the must-pays — Social Security, Medicare, you name it. For simplicity, let’s peg this at about $3.2 trillion, just as a ballpark from past trends.

– Defense: The Pentagon’s piece of the pie. Recently around $900 billion.

– Interest Expense: The cost of carrying the national debt. Let’s call it about $950 billion for a round figure.

When we plug those values into our formula we see that we have:

- Total Cash Coming In: That’s about $5.1 trillion, riding on CBO’s guesswork and last year’s haul.

- Bills We Can’t Dodge:

- Social Security: That’s gonna chew up about $1.5 trillion.

- Medicare: Tack on another cool trillion.

- Medicaid and the rest: Throw in $700 billion.

- Total Must-Pays: We’re talking about $3.2 trillion here.

- Keeping the World Safe: Defense is gonna need about $900 billion.

- Interest on the Debt: Roughly $950 billion.

What’s Left in the Kitty:

- Start with the $5 trillion.

- Subtract the non-negotiable $3.2 trillion.

- Then, the military’s $900 billion.

- Leftover Cash: About $900 billion.

Interest Coverage Ratio Reworked:

- Leftover Cash: $900 billion.

- Interest Bill: $950 billion.

- Ratio: $900 billion divided by $975 billion. You get roughly .9273

So, what does this tell us?

After Uncle Sam pays for his must-dos, he’s got to borrow funds to cover the interest on his mountain of debt. If interest rates were to increase the government would have to borrow exponentially more to make payments on the debt.

What does this tell us? With an Interest Coverage Ratio of about 0.9273, the U.S. is in a tight spot — every buck of available money after paying for essentials is getting sucked into the interest vortex. It’s like being on a financial treadmill — running hard but barely keeping up with the interest on the debt.

This isn’t just a number. It’s a neon sign flashing a warning that we’re skirting the edge of a cliff. An ICR below 1 is like a horror movie where the monster is debt, and it’s already in the house.

Economists often like to cite that since the US dollar is the reserve currency of the world that the US can simply borrow more money to pay the debt indefinitely. My response is always the same. From whom? Are you lending $$ to Uncle Sam? US government bond auctions have become the focus on Wall Street because it is tougher and tougher to make the US debt attractive. Tariffs mean that most of our trading partners will not be purchasing our debt. The grisly alternative is that Uncle Same may need to run the printing press to fund the government’s interest expenses. This is highly inflationary and perpetuates the debasement of currency.

So, there you have it — the hard truth about how the U.S. is a financial zombie, shuffling along under the weight of its debts. But remember, this is a simplification. Real life has more moving parts, and the U.S. has some tricks up its sleeve like monetary policy and new debt issuance that can keep the show running.

Now, when you peek under the hood of this American ride, what do you find? A balance sheet that screams “zombie nation.” Yeah, that’s right. Just like in those midnight horror flicks, where the dead keep walking as long as they’ve got something to munch on, the U.S. keeps chugging along as long as it can pay the interest on its gargantuan debt pile. But don’t be fooled; paying off the actual debt? That’s a story for another day — one that will never come at this rate.

Here’s the deal: the U.S. is like a guy who’s maxed out his credit cards but keeps getting his limit raised. He’s not paying them down; he’s just covering the minimum to avoid the debt collectors kicking down his door. This strategy? It’s called borrowing more dough to keep the lights on. And guess what? It’s the classic move of a zombie economy. They’re not really alive (thriving and paying down debts), but they’re not dead either (declaring bankruptcy). They’re stuck in this limbo, shuffling along, postponing the day of reckoning when the whole house of cards might come tumbling down.

Now, calling the U.S. a zombie might sound like wild talk, something you’d shout at a rowdy bar, not in a stuffy boardroom. But hey, this is the real scoop, and sometimes, the truth sounds like hyperbole. But it’s not.

So, next time you hear someone boasting about the economic might of the U.S., remember the zombie shuffle. If the credit’s cheap and the debt can be rolled over, this gig can drag on for decades. But it’s no way to run a country — not if you’re playing a long game.

It might stretch the imagination to think of the U.S. government as a zombie entity, but it’s downright chilling to see just how many stocks and publicly traded companies are shambling along in its footsteps, gorging themselves on cheap credit just to keep the lights on. It’s a macabre dance in the financial markets where the Interest Coverage Ratio (ICR) plays a pivotal role. As we’ve discussed, when a company’s ICR dips to one or below, it’s effectively joining the undead horde — zombified.

Picture this: thousands of these corporate zombies are not just surviving but are actively traded on stock exchanges every day. Most unsettling is how the world of finance and accounting often turns a blind eye. These companies might be bleeding cash and barely clinging to solvency, yet they manage to doll up their balance sheets just enough to parade through another earnings call. With a slick press release in hand, they hit the airwaves, gracing channels like Bloomberg and CNBC, proclaiming their robust health and financial vigor, deceiving the casual observer into believing they’re far from the zombie label.

It’s a facade, a clever trick with smoke and mirrors, where the true state of affairs is obscured by the glitz of well-crafted narratives. In these boardrooms, the mantra seems to be: keep the credit flowing, the press smiling, and maybe — just maybe — no one will notice the rot inside.

Zombies? Yeah, they’re not just in your favorite post-apocalyptic flick anymore, they’re walking the corridors of corporate America and the aisles of Wall Street, decked out in the latest fashion: mountains of cheap debt.

Uncle Sam, that old ringleader of reckless spending, has set such a sterling example that now, thousands of companies are getting in on the act. It’s the in thing: borrow big, because hey, why not? The dollar’s going down the tubes anyway, so you might as well load up on as much of this debased currency as you can, right?

Here’s the pitch: Corporate bigwigs and smooth-talking CFOs are selling this strategy like snake oil at a sideshow. “Money’s cheap, grab it while you can!” they croon to their boards and dazzle their investors with dazzling spreadsheets that show infinite growth. The logic seems sound on paper — borrow in a currency that’s worth less tomorrow than it is today. It’s like getting free money… or so the fairy tale goes.

But here’s where the story turns grim, folks. This isn’t a fairy tale; it’s a horror show. Many of these debt-laden companies find themselves in the red, bleeding cash with no tourniquet in sight. They’ve strapped themselves to a financial bomb, ticking away, because guess what? Borrowing stacks of cash doesn’t magically make you profitable.

And when these companies can’t turn a profit? Well, that’s when the tragedy unfolds. It’s a massacre of market value, jobs slashed, lives disrupted. This isn’t just some temporary blip on the radar; it’s a systemic infection, spreading through our economy. Each unprofitable, debt-loaded zombie company is a harbinger of wider economic decay, a sign that the financial apocalypse might just be closer than we think.

So next time you hear about a company going on a borrowing binge, remember just because zombies are fashionable, doesn’t mean they’re smart. Or safe. Or sustainable. Uncle Sam’s couture might be all the rage, but in the end, everyone knows fashion can be fatal.

These corporate cadavers are hooked on refinancing. They roll over old debts into new ones, staying just one step ahead of disaster. But this house of cards could collapse with any major shift in interest rates or a dip in investor confidence.

Here is a list that will surprise many of you. These Corporate TITANS are Zombies because their balance sheets show that they are having great struggles financing their debt.

Carnival Cruise Line (CCL) Debt Load: Over $30 billion.

Telecom Italia (TIT) Debt Load: Over €20 billion (~$21 billion USD).

Cellnex Telecom, S.A. (CLNX) Debt Load: Over €18 billion (~$19 billion USD).

Kawasaki Heavy Industries, Ltd. Debt Load: Approximately ¥1 trillion (~$9 billion USD).

Liberty Broadband Corporation (LBRDA) Debt Load: Estimated at $6 billion.

Uber Corporation (UBER) Debt Load: Over 8.3 billion.

Kohl’s Corporation (KSS) Debt Load: Approximately $5.6 billion.

Hudson Pacific Properties, Inc. (HPP) Debt Load: Around $5.5 billion.

iHeartMedia (IHRT) Debt Load: Roughly $5 billion.

AMC Entertainment (AMC) Debt Load: Approximately $5 billion.

JetBlue Airways (JBLU) Debt Load: Over $3 billion.

Wayfair (W) Debt Load: Estimated at around $3 billion.

SkyWest, Inc. (SKYW) Debt Load: Approximately $4.5 billion.

DoorDash (DASH) Debt Load: Over $2 billion.

Peloton Interactive (PTON) Debt Load: Approximately $2.3 billion.

Beyond Meat (BYND) Debt Load: Over $1 billion.

Capstone Copper Corp. (CS) Debt Load: Estimated at $1 billion.

Chewy Inc. (CHWY) Debt Load: Estimated at several hundred million dollars.

Freshpet Inc. (FRPT) Debt Load: Estimated at hundreds of millions.

Manchester United (MANU) Debt Load: Approximately £725 million (~$900 million USD).

These rankings provide a stark illustration of the significant financial challenges these companies face, emphasizing the precarious balance they must maintain to avoid bankruptcy or drastic restructuring measures.

As dollars are being debased, everything priced in that currency inflates. Toss in the complex mix of tariffs on our trading partners, and you’ve got a volatile financial cocktail — prices swing wildly, up one day, down the next, all in a desperate bid to preserve purchasing power. My perspective is shaped by my experiences, and let’s face it, my personal universe of understanding is indeed limited. That’s why I lean heavily on the giants of today’s tech: artificial intelligence, neural networks, and machine learning.

These aren’t just buzzwords; they are transformative tools that enhance decision-making. VantagePoint’s A.I. excels because it learns from failures, remembers them, and avoids them in the future, focusing instead on paths that might lead to success. This is the feedback loop that has been at the heart of every successful trader I know. Think of A.I. as your 24/7, 365-day-a-year partner in the relentless pursuit of what works.

Here’s why this should get your attention: it changes the game entirely.

It might sound straightforward, even obvious, but it’s often the obvious that traders overlook, to their detriment.

Consider the stock market. A stock might have a compelling narrative, a stellar management team, strong earnings, or unique assets and partnerships. Yet, if these positive elements aren’t reflected in the stock price, you’re caught up in what should happen, not what is happening. And banking on ‘should’ has led to more trading losses than just about anything else.

Bad traders fixate on ‘should.’ It’s a word that fills their conversations, often attached to great stories about why they’ve loaded up on a stock that’s steadily trending downwards. It’s painful to hear.

That’s where the power of A.I. and machine learning comes in. These technologies are fundamentally about recognizing patterns and using those patterns to predict the most strategic moves forward. When A.I. indicates a shift in the market, it’s something to note, even if we don’t fully grasp the underlying reasons. We might not always understand why something happens, but with VantagePoint’s A.I., we can still capitalize on it.

This is the beauty of modern trading tools, they help us navigate the complex, often mystifying waters of the financial markets with a steadier, more informed hand.

And let’s face it, the purpose of artificial intelligence is to keep you the trader on the right side of the right trend at the right time. This is priceless in today’s macro-economic environment.

Every setback teaches us something. In games of strategy like Poker, Jeopardy, Go, and Chess, A.I. has not merely competed but dominated, often eclipsing the best human players. It stands to reason that the realms of financial trading, with its complexity and reliance on predictive analytics, would be a natural domain for A.I. to excel. Here, too, A.I. is transforming the landscape, making decisions based on patterns and probabilities that might elude even the most astute human traders.

Why should trading be an exception? It isn’t. Just as A.I. has revolutionized games and strategic thinking, VantagePoint’s dual-patented artificial intelligence is making indelible marks on trading, inviting a future where financial decisions are quicker, more data-driven, and potentially more profitable than ever before.

I invite you to check it out at our next FREE live training.

Let’s be careful out there.

It’s not magic.

It’s machine learning.

THERE IS A SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.IMPORTANT NOTICE!

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.