When stock options contracts began trading in the early 1970’s they expired quarterly. Today, many options contracts expire weekly, and in the S&P 500 Index they expire three times a week on Monday, Wednesday and Friday. This creates huge opportunities for savvy traders who understand risk managed approaches to trading. In this article we’ll elaborate on the popular covered call writing strategy which offers a powerful opportunity to create additional risk managed returns in a trading portfolio.

The word “option” literally means – choice. Any time a trader purchases an option they have the choice to purchase the underlying asset at an agreed upon price, between now and the expiration date in exchange for a premium that they pay to the option seller. The option seller (creator) has created an obligation. They have accepted your premium and are obligated to make delivery of the underlying stock at the agreed upon price at expiration, should the buyer exercise their option. The easiest and simplest way to understand this concept is to think of the insurance industry. You probably have car insurance, and health insurance and property insurance. In all those instances you’re purchasing the right to protect your asset by paying the insurance company an annual premium. The insurance company on the other hand is accepting your premium and is obligated to abide by the terms of the contract.

Once you understand these distinctions, and you see how large, and powerful the insurance industry is you can begin exploring the opportunity of selling options and collecting premium. There are risks and there are rewards, and each has to be viewed in context of the probabilities.

One of the most popular trading strategies for income minded traders is referred to as a covered call writing strategy. This trading tactic appeals to traders who own the underlying stock and are looking to SELL premium to increase their returns. For example, let’s say you own 100 shares of ABC stock at $25 a share. You think it has great longer-term potential but feel that it is in a sideways channel on the charts. An income-minded trader in this instance would look to the options market and SELL a call option and collect the premium from the options buyer. Since you own the underlying stock, you are “covered” should the stock move higher. The broad majority of the time options contracts expire worthless. So, by selling that call option and collecting the premium you are engaged in a risk managed trade, where you are willing to eliminate upside potential for the obligation and premium you collect now. This is a vital concept for traders to understand because this trade advertises a “yield.” That yield allows traders to determine whether or not to take the trade.

Let me explain.

The 10-year U.S. Government Bond is yielding 1.675%. The Federal Reserve is projecting at least a 2% inflation rate. The advertised yield on a risk-free trade at present time is a “loss” of the difference between the two of -.325%. Any trader who is in the financial markets aware of this reality is comparing their returns to what the overall market is doing and offering, and this risk-free yield.

You can get a pretty good idea of what that advertised yield on a covered call is by looking at a high-quality stock and then looking at the at the money strike price at a one year expiration.

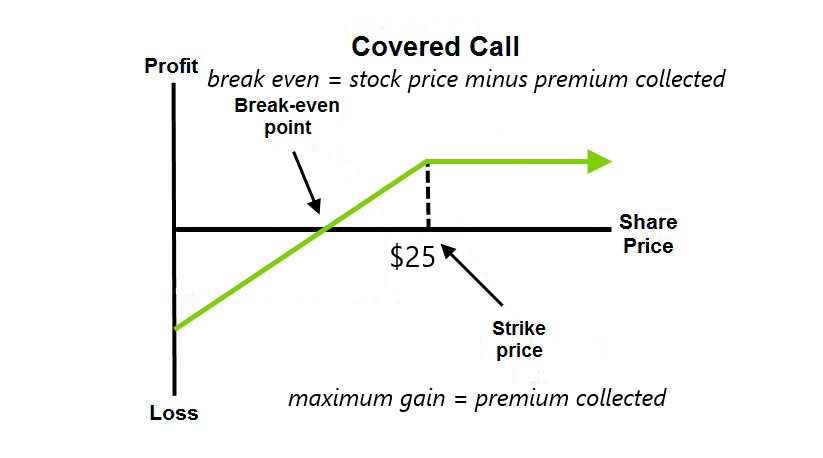

Say you own ABC stock at $25. But the $25 call option with a one-year expiration is trading at $3.5. When you divide the premium of $3.50 by the stock price that equals 14%. That is the maximum yield that a covered call writer will earn on a covered call write going one year out. That will occur if the stock price is at any price over $25 at expiration date.

That 14% maximum potential return needs to be compared to the stock’s history, its volatility and what the overall market has done to determine if this yield is attractive. This advertised yield is also always compared to the risk-free rate available for anyone who purchases a ten year bond.

But there is one more powerful feature of the covered call write that makes it very attractive for income minded traders. When you subtract the premium collected from the current stock price that is the downside breakeven price. What this means is that since you own the stock at $25, if you sell the call option going out one year for $3.5, this means that the stock could fall to $21.50 at expiration before you would experience any loss of on this particular trade. In other words, the stock could fall 14% before you were adversely affected.

The following chart illustrates what the potential outcomes of the Covered Call Write are.

This strategy is implemented tens of thousands of times a day by traders and investors who understand the risk/reward potential for this type of trade. The actual yield will only be known at the options expiration date.

What a covered call write trader is saying is that they are willing to give away upside potential now for the premium/yield that they can lock in today. Since they own the stock, once they collect the premium, they readjust their cost basis on the stock by subtracting the amount of premium they collect. This practice determines the break-even price of the stock. The risk to a covered call write as the graphic depicts is clearly to the downside.

Seasoned traders will apply this same logic to the weekly options expirations. It’s not uncommon for traders to earn 1% to 3% weekly on these types of trades. This will occur whenever the stock expires at or above the “at the money” strike price when the trade was initiated. At any price below the “at-the-money” strike price the yield is less. At any price below the break-even price a trader would experience a loss and a negative yield.

When you genuinely understand this trade and its math you begin to understand how every asset is advertising a maximum risk managed yield. You as a trader can then determine if that yield is worth your time and energy to pursue. The actual yield will only be known at expiration and will depend completely upon where the stock is trading on the expiration date.

Option expiration opportunities depend on the interest and popularity of the underlying stock. Stocks like Apple (AAPL) will have weekly expirations, while lower-volume small-cap stocks may have only quarterly expirations available.

The most common expiration periods available are:

- Quarterly: Quarterly options expire on the third Friday in the last month (March, June, September, December) of every quarter. Traders call this date “quadruple witching” because stock options, index futures, single stock futures, and stock index options simultaneously expire. To calculate the maximum advertised yield on a quarterly option simply multiply the “at-the-money” call option premium by four. That will provide an annualized amount which needs to be compared to the price of the stock.

- Monthly: Monthly options expire on the third Friday of every month. To calculate the maximum advertised yield on a monthly options simply multiply the “at-the-money” call option premium by twelve. That will provide an annualized amount which needs to be compared to the price of the stock.

- Weekly: Options that expire on stocks every Friday are known as “weeklies.” These weekly options usually only go out two months. To calculate the maximum advertised yield on a weekly options simply multiply the “at-the-money” call option premium by 52. That will provide an annualized amount which needs to be compared to the price of the stock.

- Intra-week: High-volume names like the SPDR S&P 500 ETF Trust (SPY) will have multiple expirations during a week. Intra-week options expire on Mondays and Wednesdays, on top of the Friday weekly options.

- LEAPS: Options with expiration dates that go out up to three years are known as Long-term Equity AnticiPation Securities.

This strategy is amongst the most popular trading tactics today because of its simplicity and how it attractively manages a large part of risk on a trade.

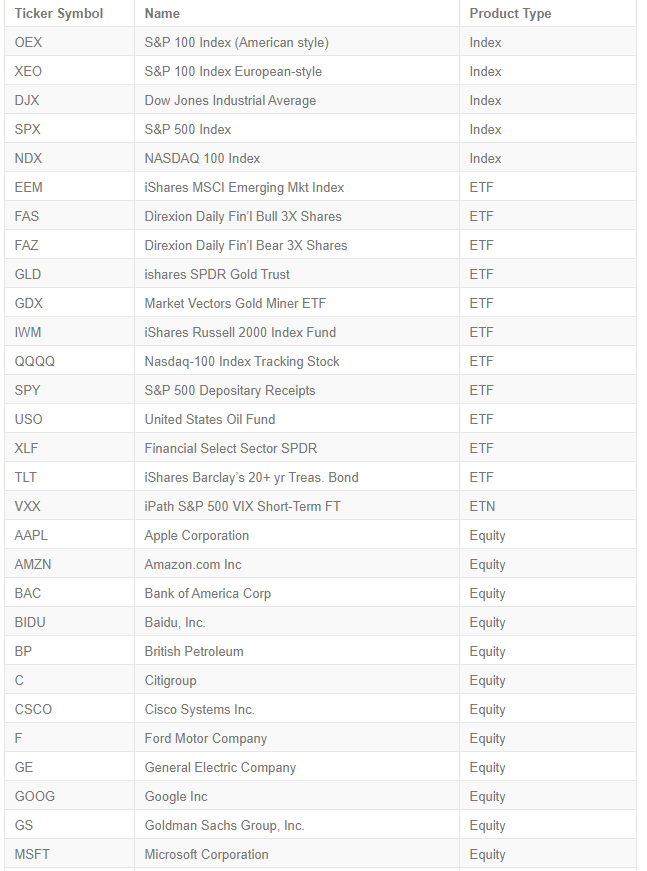

Here is a listing of assets offering weekly options expirations. This tactic is how many professional traders harness volatility by giving away upside for an attractive yield as long as the asset does not trade below the break-even point at the expiration date.

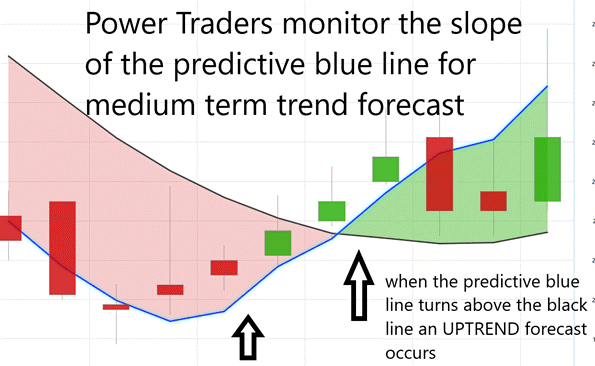

VantagePoint Power Traders use this understanding by cross-referencing an a.i. forecast with the inherent power and potential leverage of a covered call write.

We publish a weekly stock study which you can learn more about by clicking here, here and here. In these articles we show how artificial intelligence creates a medium-term forecast, clearly defines a “value zone,” and provides a predictive daily high and low price.

When an “Up Opportunity” occurs one of the first trade opportunities worth evaluating is an at-the-money-covered call write. This strategy allows traders who understand this concept and the risk and reward which clearly define it, allow a trader to quickly create a risk-advantaged trade. What I mean by this, is that all of trading can be reduced to the following two questions:

What if I’m right?

What if I’m wrong?

In a covered call write tactic the boundaries for profitability and the probability of success are clearly in the traders favor as long as the underlying asset stays above the break-even point at expiration. It is not risk-free by any means, but you will appreciate the power of this concept when the market moves against you in a covered call write, and you still do not lose any money. Mathematically speaking this is the ideal that traders aspire to.

Great traders look for consistency in their trading results.

I track all of my trades and every hundred trades I develop my metrics.

What was my average winning trade?

What was my average losing trade?

What was my biggest win?

What was my biggest loss?

This discipline has been necessary for me to develop an understanding of what it takes to be successful in trading. By doing this I have developed huge confidence in my abilities. This confidence has been a result of tens of thousands of trades and learning from my mistakes.

Trading is largely defensive. If you take care of losers as a top priority, the winners will take care of the rest.

In trading you have to become expert at taking losses, and not looking back. Recognize that your ego is the enemy, and then taking losses becomes an essential part of the activity.

Risk is, by definition, the threat of loss due to uncertainty.

Think about your own losing trades and ask yourself what did you learn from that experience? What is your method for analyzing risk?

Are you capable of finding those markets with the best risk/reward ratios out of the thousands of trading opportunities that exist?

Artificial intelligence is not “a would be nice to have” tool.

It is an “absolutely must-have” tool to flourish in today’s global markets.

Intrigued? Visit with us and check out the A.I. at our Next Live Training.

It’s not magic. It’s machine learning.

Make it count.

THERE IS SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.IMPORTANT NOTICE!

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.